https://doi.org/10.22267/rtend.26272.295

Accounting and international standards

Initial adoption of IFRS 16 in Colombia: evidence from a case study

Adopción inicial de la NIIF 16 en Colombia mediante estudio de caso

Adoção inicial da IFRS 16 na Colômbia: evidências de um estudo de caso

By: Mario Andrés Peña Duarte![]() 1;Ricardo Jesús Guerrero Díaz

1;Ricardo Jesús Guerrero Díaz![]() 2;Miguel Antonio Piñerez Flórez

2;Miguel Antonio Piñerez Flórez![]() 3

3

1Master’s Degree in Corporate Finance, Universidad de Santander, Full-time professor, Universidad Popular del Cesar Seccional Aguachica. ORCID: 0000-0002-3362-0586. E-mail: mandrespena@unicesar.edu.co, Aguachica - Colombia.

2 Master’s Degree in Taxation and Fiscal Policy, Accounting, Finance and Taxation, Universidad de Medellín, Professor, Universidad Popular del Cesar Seccional Aguachica. ORCID: 0000-0002-1270-6989. E-mail: ricardoguerrero@unicesar.edu.co, Aguachica - Colombia.

3 Master’s Degree in Accounting Sciences, Accounting and Finance, Universidad Santo Tomas, Ad Honorem Adjunct professor, Universidad Popular del Cesar Seccional Aguachica. ORCID: 0009-0001-6406-4324. E-mail: miguelpinerez@unicesar.edu.co, Aguachica - Colombia.

Received: September 30, 2025 Accepted: June 1, 2026

DOI: https://doi.org/10.22267/rtend.26272.295

How to cite this article: Peña, M., Guerrero, R. & Piñerez, M. (2026). Initial adoption of IFRS 16 in Colombia: Evidence from a case study. Tendencias, 27(2), 1-31. https://doi.org/10.22267/rtend.26272.295

![]()

Abstract

Introduction: IFRS 16 substantially changed lease accounting by requiring the recognition of right-of-use assets and lease liabilities, replacing the previous treatment of certain operating leases as period expenses. Objective: To analyze the accounting and financial impacts of the initial adoption of IFRS 16 in a private organization operating in the productive sector. Methodology: This research adopts a qualitative approach through a case study and documentary analysis of contracts, accounting policies, financial statements, measurement calculations, and tax reconciliations. Results: The adoption of the standard resulted in the recognition of right-of-use assets and lease liabilities, as well as impacts on deferred taxes, tax reconciliations, and financial indicators. Furthermore, it made visible contractual obligations that had not previously been reflected on the balance sheet. Discussion: The findings indicate that IFRS 16 enhances financial transparency; however, it also requires greater technical rigor in determining discount rates, assessing materiality, measuring lease contracts, and preparing disclosures, particularly due to its effects on EBITDA, leverage, and profitability. Conclusion: IFRS 16 transforms the accounting and financial management of leases by strengthening the traceability of assets, liabilities, and contractual risks.

Keywords: contractual agreement; property rights; financial statements; financing; taxes; leases.

JEL: G12; G14; M40; M41; M48; M49.

Resumen

Introducción: La NIIF 16 modificó sustancialmente el reconocimiento de los arrendamientos al exigir el registro de activos por derecho de uso y pasivos por arrendamiento, superando el tratamiento previo de ciertos arriendos operativos como gastos del periodo. Objetivo: Analizar los impactos contables y financieros de la adopción inicial de la NIIF 16 en una organización privada del sector productivo. Metodología: La investigación se desarrolla bajo enfoque cualitativo, mediante estudio de caso y análisis documental de contratos, políticas contables, estados financieros, cálculos de medición y conciliaciones tributarias. Resultados: La adopción de la norma genera reconocimiento de activos por derecho de uso y pasivos por arrendamiento, impactos en impuestos diferidos, conciliaciones fiscales e indicadores financieros; además, visibiliza obligaciones contractuales que antes no se reflejaban en el balance. Discusión: Los hallazgos evidenciaron que la NIIF 16 mejora la transparencia financiera, pero exige mayor rigor técnico en la determinación de tasas de descuento, materialidad, medición de contratos y revelaciones, especialmente por sus efectos en EBITDA, endeudamiento y rentabilidad. Conclusión: La NIIF 16 transforma la gestión contable y financiera de los arrendamientos, fortaleciendo la trazabilidad de activos, pasivos y riesgos contractuales.

Palabras clave: acuerdo contractual; derechos a la propiedad; estado financiero; financiación; impuestos; arrendamientos.

JEL: G12; G14; M40; M41; M48; M49.

Resumo

Introdução: A IFRS 16 alterou substancialmente o reconhecimento das locações, ao exigir o registo de ativos por direito de uso e passivos por locação, superando o tratamento anterior de certas locações operacionais como despesas do período. Objetivo: Analisar os impactos contabilísticos e financeiros da adoção inicial da IFRS 16 numa organização privada do setor produtivo. Metodologia: A investigação desenvolve-se sob uma abordagem qualitativa, através de um estudo de caso e de uma análise documental de contratos, políticas contabilísticas, demonstrações financeiras, cálculos de mensuração e reconciliações fiscais. Resultados: A adoção da norma gera o reconhecimento de ativos por direito de uso e passivos por arrendamento, impactos nos impostos diferidos, reconciliações fiscais e indicadores financeiros; além disso, torna visíveis obrigações contratuais que anteriormente não se refletiam no balanço. Discussão: Os resultados evidenciaram que a IFRS 16 melhora a transparência financeira, mas exige maior rigor técnico na determinação de taxas de desconto, materialidade, mensuração de contratos e divulgações, especialmente devido aos seus efeitos no EBITDA, endividamento e rentabilidade. Conclusão: A IFRS 16 transforma a gestão contabilística e financeira das locações, reforçando a rastreabilidade de ativos, passivos e riscos contratuais.

Palavras-chave: acordo contratual; direitos de propriedade; demonstração financeira; financiamento; impostos; arrendamentos.

JEL: G12; G14; M40; M41; M48; M49.

Introduction

International Financial Reporting Standards (IFRS) are continuously updated to address changes in the business and regulatory environment. In 2019, IFRS 16 introduced significant changes to the recognition, measurement, and presentation of leases. Its primary objective was to require the recognition of leases through right-of-use assets and corresponding lease liabilities arising from contractual payment obligations. Prior to the implementation of IFRS 16, operating leases were generally not recognized on the statement of financial position and were instead recorded as expenses in the statement of profit or loss. IFRS 16 applies to financial statements prepared on or after January 1, 2019, in Colombia and internationally (Martínez, 2018). Subsequently, the standard was amended to address lease concessions and rent reductions that may affect financial reporting (Romero, 2021). The objective of this article is to analyze the accounting and financial impacts resulting from the initial adoption of IFRS 16 through a case study of a manufacturing-sector company that implemented the standard in 2019. Given the importance of lease transactions to the entity's operations, their management requires rigorous oversight by the finance department. The study is based on a documentary analysis of the implementation process observed by the authors.

Literature review

The lease accounting literature distinguishes between operating leases and finance leases. This distinction is important because it influences both financing decisions and the financial metrics used by different stakeholders. Christensen et al. (2025) found that the adoption of IFRS 16 significantly reduced the volume of operating leases reported in financial statements. They also showed that some companies, particularly those most sensitive to financing costs, modified the terms of their lease agreements by shortening contractual lease periods. The authors argue that companies may adjust the duration and timing of lease contracts in order to influence their accounting recognition.

In their study, Molina et al. (2025) argue that there is ambiguity regarding what exactly constitutes the “obligation” that must be recognized as a lease liability under IFRS 16, particularly whether such a liability arises from contracts that are already in force. The authors also identify ambiguities concerning the derecognition of these liabilities under the requirements of IFRS 9.

In the study by Delgado et al. (2023), it was observed that determining the incremental borrowing rate requires an assessment of both the nature of the leased asset and the lease term. Under certain circumstances, the relevant data may be directly observable; however, the literature provides limited guidance and does not offer examples of models for estimating the incremental borrowing rate when lease contracts contain specific or unusual contractual features. Furthermore, Lopes and Penela (2025) argue that the implementation of IFRS 16 affects key liquidity and leverage indicators, while also impacting return on equity (ROE) and earnings per share.

In the analysis conducted by Rojas and Franco (2022) of the financial reports of 100% of all publicly listed companies in Colombia, the most significant impacts were found to stem from reclassifications made in financial reporting, effects on equity, and deficiencies in disclosure requirements. According to the study conducted by Callo et al. (2025) IFRS 16 may affect business valuation exercises because the new valuations influence financial statements and, consequently, the various valuation methods applied. This is due to the standard’s requirement for careful adjustments to the financial ratios used in valuation analyses.

Methodology

The methodological approach is qualitative and aims to understand, describe, and document the experience of implementing IFRS 16 in a private sector organization. A non-experimental research design was adopted because no variables were manipulated; instead, the study examined a phenomenon that had already occurred, namely the adoption of IFRS 16. Furthermore, the study is descriptive, detailing the implementation process of International Financial Reporting Standard (IFRS) 16 and its implications for accounting management. In addition, it is structured as a case study focusing on a company that adopted the standard. The population consists of companies required to apply full IFRS in Colombia, while purposive sampling was employed to select a single representative case. The methods used to analyze the data were content and document analysis, complemented by a comparison of financial statements. Access to the information was obtained through an accounting consulting engagement conducted by the authors. The materials analyzed included contracts, financial reports, accounting policies, Excel spreadsheets, working meetings, and off-balance-sheet reports. To preserve confidentiality, the real name of the entity is not disclosed, and it is referred to throughout the study as “Energías Limpias Sociedad BIC” (a pseudonym), a clean-energy production company located in eastern Colombia that operates its plant on the premises of its parent company under a lease agreement. The company’s identity has been withheld to protect confidentiality and ensure that the information is used solely for academic purposes.

Results

IFRS 16 establishes that, as a general principle, leases include the following types: finance leases, operating leases, and sales followed by finance leases (Tejada, 2017). In the case of finance leases, the lessee recognizes, measures, presents, and discloses the leased asset as property, plant, and equipment or another category of asset, with the corresponding financial liability; in the case of operating leases, the lessee does not recognize the asset and, consequently, no change is reflected in its statement of financial position (Ramirez, 2019).

Prior to the adoption of IFRS 16 lease accounting was governed by International Accounting Standard (IAS 17) “Leases,” which was replaced in 2019. According to Barral et al. (2014), IAS 17 had not undergone major changes since its introduction in 1982 and was largely inspired by the 1976 Statement of Financial Accounting Standards (FAS 13). Under the previous lease accounting model established by IAS 17 leases were first classified as either finance or operating leases. This classification determined their recognition, measurement, and presentation in financial statements. The standard established that a lease should be classified as finance lease when it substantially transferred the risks and rewards associated with ownership; otherwise, it was classified as an operating lease.

IAS 17 was the accounting standard in effect until December 31, 2018, governing the recognition, measurement, presentation, and disclosure of lease transactions. The standard was primarily based on the classification of leases as either finance leases and operating leases for both lessors and lessees, depending on the specific circumstances of each contract (Alzate, 2019). Under IAS 17, the accounting treatment of a lease depended on its classification. The accounting treatment and recognition of operating leases were considerably simpler than those of finance leases, in essence, lease payments were recognized by lessees as expenses over the term of the lease agreement (Carrillo, 2013).

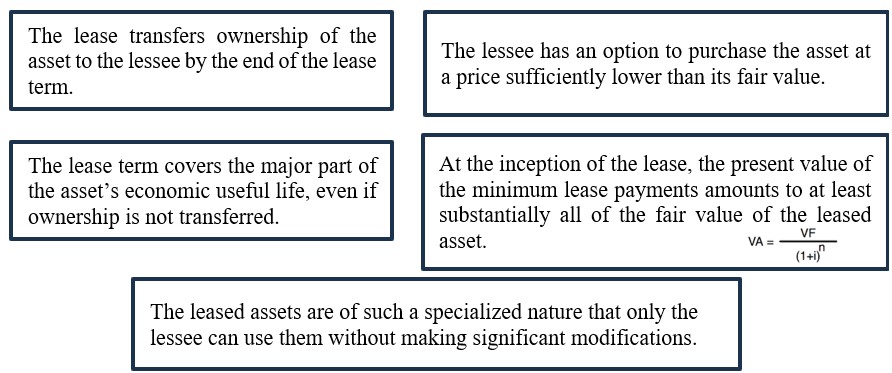

This type of lease was not previously recognized as either an asset or liability in the entity’s statement of financial position. However, when a lease was classified as a finance lease, it was initially recognized in both assets and liabilities at the lower of the fair value of the asset and the present value of minimum lease payments. This approach allows the transaction to be reflected in the statement of financial position, rather than limiting it solely to recognition as an expense in income (Carrillo, 2013). In practice, IAS 17 established a number of principles for determining whether a lease should be classified as a finance or an operating lease. This assessment was based on the transfer of risks and rewards associated with ownership of the asset. To support this determination, the standard identified five principal indicators: transfer of ownership, a bargain purchase option, lease term, the present value of minimum lease payments, and the existence of specialized assets. Depending on the outcome of this assessment, the lease agreement would be classified accordingly. It should be noted that a preparer of financial statements could classify a lease as a finance lease based on the presence of any one of these indicators or a combination of several. IAS 17 formed part of the full IFRS framework, which in Colombia applies to Group 1 entities. In the IFRS for Small and Medium-sized Entities (IFRS for SMEs), the principles governing the recognition, measurement, and presentation of leases are very similar to those established in IAS 17; accordingly, the IFRS for SMEs include Section 20, Leases. Under the IFRS for SMEs, an operating lease is an agreement whereby the lessor grants the lessee the right to use an asset for a specified period in Exchange for a payment or a series of lease payments. The lessor accounts for the asset as property, plant and equipment and depreciates it over its useful life in accordance with entity’s accounting policies (Orozco, 2015). Based on the provisions of IAS 17 and section 20 of the IFRS for SMEs, leases are recognized and measured according to the following principles: leases are classified as either finance leases or operating leases; finance leases are recognized when they meet the lease classification criteria established by the standard; and operating leases are recognized as a straight-line expense that does not affect the statement of financial position, regardless of the lease term or the type of asset involved. Figure 1 presents the lease classification test established under IAS 17, the international accounting standard on lessees that has since been superseded by IFRS.

Figure 1

Tests under the superseded International Accounting Standard 17 (IAS 17)

Source: Own elaboration.

It is important to note that Section 20 of the IFRS for SMEs and IAS 17 were in force until 2018 and were replaced by IFRS 16 as of 2019. Currently, Section 20 of the IFRS for SMEs has not been aligned with IFRS 16 and instead remains more closely aligned with the criteria previously established under the now-superseded IAS 17 and the interpretations IFRIC 4, SIC-15, and SIC-27 (Varón, 2023).

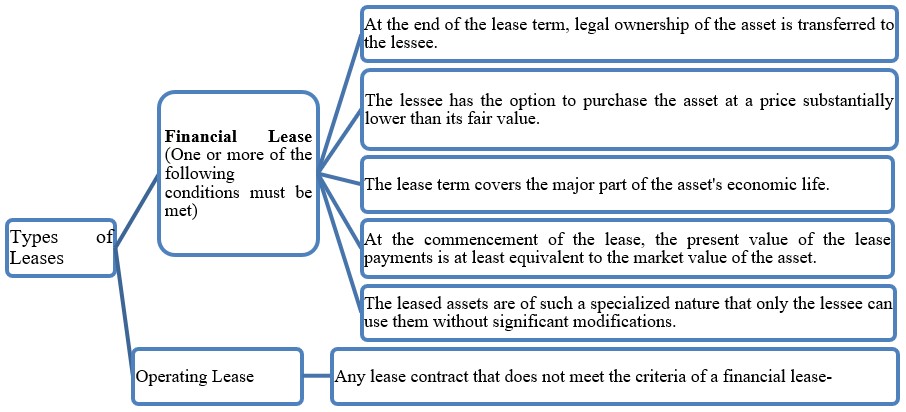

Unlike IAS 17 and section 20, IFRS 16 provides a single accounting model for lessees, requiring them to recognize asset and liabilities for all lease contracts on their statement of financial position, unless the contractual term is less than 12 months or the underlying asset qualifies as a low-value asset (Armijo, 2019). This raises the following question: why should the structure provided by IAS 17 with its assessment test for finance or operating leases be changed? To address this question, consider the following scenario: an entity leases a number of premises for the sale of its merchandise nationwide; the properties are leased under operating lease contracts with an average term of three years. The leased assets have a high cost for the entity, which opts to lease them because acquisition is not financially viable.

If these contracts are evaluated under the five indicators of IAS 17 or Section 20 of the IFRS for SMEs, the conclusion would be that none of the five finance lease recognition criteria are met: there is no transfer of ownership, no bargain purchase option, the lease term does not cover the majority of the asset's economic life, the present value of minimum lease payments does not represent substantially all of the fair value of the leased asset, and the assets are not so specialized as to preclude their use by third parties without significant modification. Consequently, the lease would be classified as an operating lease under IAS 17.

Under the operating lease model of IAS 17, these contracts would be disclosed in the income statement as an expense over each contract period, without any recognition on the balance sheet. However, in the context of an operating lease, a different situation becomes apparent: the existence of a financial lease liability over a three-year non-cancellable contractual commitment. This illustrates a widely recognized shortcoming of IAS 17's accounting model, which has been criticized primarily on the grounds that operating leases should give rise to the recognition of assets and liabilities in the lessee's financial statements, thus reflecting the existence of two very different models for leases finance and operating on the statement of financial position. As a result, similar transactions could be recognized and presented in very different ways (Salazar et al., 2015). According to Molina and de Vicente (2016), IFRS 16, with its single lease model, originates in the recognition of a liability that was being omitted; companies were not disclosing their actual indebtedness. This structural change entails not only the appearance of a liability, but also the simultaneous recognition of a right-of-use asset on the statement of financial position. According to Barral (2014), the key to this recognition lies in the change of the unit of account for identifying a resource as an asset a resource that arises from the right to use an asset under the contract. This new model of recognizing right-of-use assets is consistent with the dramatic growth of intangible capital, which is becoming the principal creator of value (Lev, 2017). IFRS 16 thus aligns with the growing need to strengthen the accounting recognition of rights that were previously not presented as assets.

The essence of IFRS 16 is to avoid undervaluing the indebtedness arising from non-cancellable lease contracts and to reflect the rights to use significant assets. For this reason, the IASB replaced IAS 17 with IFRS 16, under which no distinction is made between finance and operating leases: a right-of-use asset and a corresponding liability must be recognized for any type of lease at the present value of the unavoidable cash flows (Mora, 2021). IFRS 16 does permit one exception: lessees may elect not to recognize rights and obligations on the statement of financial position for contracts where the lease term is less than one year and the underlying asset is of a non-material amount. In such cases, the lease is treated as an operating contract, with only the lease expense recognized in profit or loss. Studies on the impacts of IFRS 16 conclude that the standard changes the perception of indebtedness and financial structure, generating challenges for financial analysis and decision-making (Lopes & Penela, 2024). Although IFRS 16 standardizes accounting criteria, it has differentiated effects depending on the economic context of each sector. For example, in companies with high volumes of lease agreements, such as mining companies, Cueva et al. (2025) found that the capitalization of lease expenses as right-of-use assets alters firms’ financial structure, which in turn may affect their credit risk and financing conditions.

The application of IFRS 16 aims to eliminate any practice that allow liabilities arising from operating leases to remain off the balance sheet. According to Delgado et al. (2022), this promotes greater transparency and comparability in the financial statements of companies. The most recent amendment to IFRS 16, introduced by the IASB in response to the COVID-19 crisis, allowed companies to manage unforeseen events and adjust accounting requirements to new circumstances. This amendment simplified the application of the standard, reducing costs and complexity by offering lessees the option to not treat COVID-19-related rent concessions as lease modifications (Moscariello & Pizzo, 2021).

IFRS 16 has been in force in Colombia since its incorporation into the national regulatory framework through Decree 2170 of 2017, which added Annex 1.3 to the Unified Regulatory Decree (DUR) 2420 of 2015. This annex came into effect on January 1, 2019 (Ramírez, 2017). Subsequently, Decree 2483 of 2018 compiled the technical normative frameworks for Groups 1 and 2, placing IFRS 16 in Technical Compilation Annex 1 for Group 1 entities. IFRS 16 applies to general-purpose financial statements of Group 1 entities prepared from 2019 onwards (Ramírez, 2019).

Case study: “Energías Limpias Sociedad BIC”

“Energías Limpias Sociedad BIC” first applied IFRS 16 on January 1, 2019. Its corporate purpose is the operation and commercialization of biofuel production plants. It belongs to the group of Group 1 financial reporting entities and established its production operations on the premises of its parent company in eastern Colombia. The facilities where the entity's plant and its administrative offices operate are subject to an operating lease agreement. For this case study, the following sequential steps were established: Step 1, evaluate the lease contract; Step 2, recognize the lease conditions; Step 3, determine the discount rate; Step 4, calculate the contracts and record accounting entries; Step 5, prepare the accounting and tax reconciliation of the contracts; Step 6, analyze other considerations (cash flows, EBITDA). In this case, Table 1 presents the figures in thousands of Colombian pesos.

Table 1

Contract Inventory – Energías Limpias Sociedad BIC

Contracts |

Entity |

Contract date |

Term |

Years remaining |

Annual amount |

Renewal probability |

Implicit rate |

Incremental rate |

Materiality threshold |

CTA 001 |

Matriz s.a. |

1/01/2016 |

37 years |

34 years |

$ 600.000 |

Cannot be determined |

N/A |

7,51% |

$ 130.000 |

CTA 002 |

Mapa s.a.s |

1/01/2016 |

10 years |

7 years |

$ 132.000 |

Yes, same term |

N/A |

7,51% |

$ 130.000 |

Source: Own elaboration.

Contract CTA 001 is executed with the parent company, under which one hectare of land on which the production plant operates is leased; the contract is adjusted annually in accordance with the Consumer Price Index (CPI) on January 1 of each year. The contract clauses establish that any improvements made on the premises (production plant) shall remain the property of the parent company. Contract CTA 002 is executed with “Inmobiliaria Mapa SAS”; these premises house the company's administrative headquarters. The contract stipulates that, upon termination, the company must return the premises in the same condition as when they were handed over. For the purposes of this article, only Contract CTA 001 will be analyzed.

Step 1: legal evaluation of the lease contract

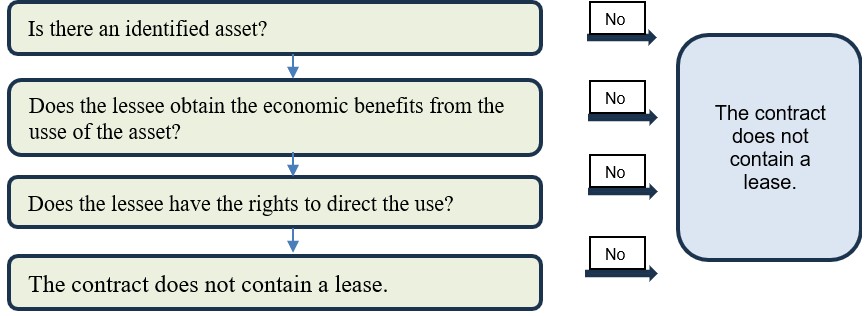

Article 1973 of the Civil Code defines a lease as a contract whereby the parties bind themselves reciprocally: one party grants the other the enjoyment of an asset, performs a work, or renders a service, and the other pays a determined price for such enjoyment, work, or service (Código Civil, Artículo 1973; “C-293 de 2024 – Relatoría ANCP-CCE”). Additionally, paragraph 9 of IFRS 16 establishes the criteria for determining whether a contract constitutes a lease: a contract is classified as a lease if it involves an identifiable asset and transfers the right to control its use for a specified period in exchange for economic consideration. Paragraphs B9 to B31 of IFRS 16 provide detailed guidance for evaluating whether a contract is, or contains, a lease (IFRS, 2018).

This regulation is consistent with the Civil Code, as the central element is the enjoyment of an identifiable asset, which constitutes the principal characteristic distinguishing a lease from a service agreement (Figure 2).

Figure 2

Transaction type assessment test

Source: Own elaboration.

Under the proposed evaluation criteria, the contracts executed revolve around an identifiable asset; the company limits the legal owner's use thereof, as it will control the asset for the agreed period. This distinction is important to establish at the outset in order to differentiate a lease contract from a service agreement.

Step 2: lease recognition

In accordance with IFRS 16, and after applying the relevant test considering the lease commencement date, Energías Limpias Sociedad BIC will recognize a contract under this standard only if the following two conditions are met (Table 2):

Table 2

Evaluation of Lease Recognition Criteria under IFRS 16

Indicators |

Yes |

No |

Comments |

The lease term exceeds one year |

X |

|

The contract with Casa Matriz is set for 46 years; for the administrative offices, the contract is set for 10 years. |

The underlying asset is material to the company (the fair value of the asset exceeds the materiality threshold established for leases). |

X |

|

The land where the plant operates and the administrative offices are considered material assets to the company, given the importance of these assets to operations and their fair values, which exceed the established materiality threshold. |

Source: Own elaboration.

Regarding the materiality policy (Table 3), the established relative importance threshold is considered an essential qualitative characteristic of useful financial information (Peña, 2021). The definition of materiality is found in paragraph CC11 of the Conceptual Framework for Financial Reporting, which states that information is material if its omission or misstatement could influence the decisions that users make on the basis of financial statements (IFRS, 2018).

According to Ariza and Peña (2023), the application of materiality involves professional judgment on the part of the financial reporting preparer. Materiality may be established at different levels: general materiality and specific materiality. Specific materiality is lower than general materiality and is used in the case study to limit the scope to significant assets controlled under lease contracts that fall within the scope of IFRS 16.

The materiality principle in the implementation of IFRS 16 is reflected in the recognition exemptions: a lessee may elect not to apply the standard's requirements to short-term leases or those whose underlying asset is of low value. The standard identifies examples of low-value assets such as tablets, personal computers, small items of office furniture, and communication equipment, without establishing precise criteria for determining the materiality of underlying assets. Accordingly, this assessment is based on the guidance of the Conceptual Framework and the exercise of professional judgment (IFRS, 2018).

In the case study, the entity defined specific materiality for underlying assets in lease contracts at a value equal to or greater than 1.5% of fixed assets. At the close of the period ending December 31, 2018, this 1.5% equaled COP $130,000. This threshold is compared with the fair value of the leased assets: if the fair value of the asset exceeds the specific materiality threshold, the contract falls within the scope of IFRS 16; otherwise, if the fair value is below the threshold, the lease is recognized directly in profit or loss as a straight-line expense over the contract period.

Step 3: Determination of the discount rate

An assessment was made of whether to apply the interest rate implicit in the lease or, alternatively, the lessee's incremental borrowing rate. According to the Internatonal Accounting Standards Board (2016), the implicit rate is the rate that equates the present value of the lease payments and unguaranteed residual value with the sum of the fair value of the underlying asset and the lessor's initial direct costs.

In the case of Energías Limpias Sociedad BIC, this rate cannot be determined reliably, as the contracts evaluated do not represent a financed acquisition of the asset and do not include transfer of legal title at the end of the contractual period. Therefore, measurement must be performed using the incremental borrowing rate, understood as the rate the entity would have to pay to obtain financing, under comparable terms of duration, collateral, amount, and risk, to acquire an asset with characteristics equivalent to the right-of-use asset. In practice, this rate can be estimated through bank quotes for financing similar assets or based on the weighted average cost of existing credits intended for the acquisition of fixed assets. The main technical difficulty lies in estimating the fair value of the underlying asset, as lessees do not always have sufficient observable information to perform such measurement (Morales & Zamora, 2018).

This rate reflects lease contracts that are not intended to result in the acquisition of the asset that is, operating leases (International Accounting Standards Board, 2016). To determine the incremental rate, Energías Limpias Sociedad BIC obtained quotes from financial institutions for the cost of a loan to acquire fixed assets, or alternatively, calculated the weighted average cost of existing financial obligations related to asset purchases. The weighted rate of 7.51%, shown in Table 3, was used as the incremental interest rate.

Table 3

Summary of financial liabilities as of december 2018

Financial liabilities |

Amount |

Annual effective rate (AER) |

Working capital credit |

$ 1.680.000 |

11,00% |

Treasury credits |

$ 1.300.000 |

10,50% |

Credit for asset improvement |

$ 3.450.000 |

6,90% |

Credits for asset purchases |

$ 2.200.000 |

8,10% |

Leasing credit for machinery purchase |

$ 4.250.000 |

7,70% |

Total |

$12.880.000 |

|

Source: Own elaboration.

The standard establishes that the incremental borrowing rate takes into account the rates applicable to the financed acquisition of assets (Díaz, 2018). For the case study, leasing credits and other obligations related to long-term asset acquisitions are included, as presented in Table 4, which shows the weighted rate of existing credits for the acquisition of fixed assets.

Table 4

Weighted rate of existing credits for fixed asset purchases

| Financial liabilities December 2018 |

Amount |

Rate EA |

% Amount |

Weighted rate |

|---|---|---|---|---|

Credit for asset improvement |

$3.450.000 |

6,90% |

35% |

2,40% |

Credits for asset purchases |

$2.200.000 |

8,10% |

22% |

1,80% |

Leasing credit for machinery purchase |

$4.250.000 |

7,70% |

43% |

3,31% |

Asset purchase obligations |

$9.900.000 |

|

|

7,51% |

Source: Own elaboration.

The resulting weighted rate of 7.51% will be referenced as the incremental interest rate. This rate will be used to discount lease payments in accordance with the contract term, which may include successive renewals or extensions. It should be noted that this process applies only when the fair value of the asset exceeds the specific materiality threshold and the contract term, including possible renewals, exceeds 12 months.

Step 4: contract calculation and accounting recognition

The initial value of the right-of-use asset was determined. According to Ramírez (2019), the value of the lease liability must first be determined; in accordance with paragraph 26 of IFRS 16, this corresponds to the present value of fixed and variable lease payments that have not been paid at the commencement date. These are discounted using the interest rate implicit in the lease, if that rate can be readily determined; if not, the lessee applies its incremental borrowing rate, as shown in Table 5, Lease Agreement CTA 001: Plant Property Lease.

Table 5

Conditions of contract CTA 001 for estimating future cash flows

Contract CTA 001 |

|

Start |

1/01/2016 |

End |

31/12/2053 |

Years |

37 |

Remaining years |

34 |

Annual payment 2019 |

$ 600.000 |

Incremental discount rate |

7,51% |

Present value of payments |

$7.441.111 |

Source: Own elaboration.

Table 6 presents the calculation of the amortized cost of the lease liability and the depreciation of the right-of-use asset, showing the year-by-year amortization of the debt and the periodic consumption of the asset.

Table 6

Amortized cost of the obligation and depreciation of the right-of-use-asset

| Lease Liability |

|

|

|

Right-of-Use Asset |

||||

|---|---|---|---|---|---|---|---|---|

| Period |

Amount |

Interest |

Payment |

Amortization |

Balance |

Amount |

Depreciation |

Balance |

2019 |

$ 7.441.111 |

$ 558.835 |

$ 600.000 |

$ 41.165 |

$ 7.399.946 |

$7.441.111 |

$ 201.111 |

$7.240.000 |

2020 |

$ 7.399.946 |

$ 555.743 |

$ 600.000 |

$ 44.257 |

$ 7.355.690 |

$7.240.000 |

$ 201.111 |

$7.038.889 |

2054 |

$ 1.077.189 |

$ 80.898 |

$ 600.000 |

$ 519.102 |

$ 558.087 |

$ 402.222 |

$ 201.111 |

$ 201.111 |

2055 |

$ 558.087 |

$ 41.913 |

$ 600.000 |

$ 558.087 |

$ 0 |

$ 201.111 |

$ 201.111 |

$ 0 |

Source: Own elaboration.

Table 7 presents the initial accounting entry for the contract, in which the right-of-use asset and the lease liability are recognized simultaneously.

Table 7

Recognition of Contract CTA 001 – Adoption Date: January 1, 2019

Concept |

Debit |

Credit |

Right-of-use asset |

$7.441.111 |

|

Lease liability |

|

$7.441.111 |

Source: Own elaboration.

The initial application of IFRS 16 offers three alternatives for the implementing entity:

- Retrospective application (full retrospective approach): in accordance with paragraph C5(a) of IFRS 16.

- Modified retrospective approach: in accordance with paragraph C5(b) and paragraphs C7 to C13 of IFRS 16.

- Modified retrospective approach with practical simplification: in accordance with paragraph C8(b)(ii) of IFRS 16.

Alternative 1 requires the preparation of pro forma financial statements, including comparative information for the period preceding adoption. In the case study, the impact would have had to be projected from 2018 if this method had been selected. The retrospective approach is intended to disclose the comparative effects of implementing the standard. Alternative 2 requires recognizing the cumulative effect of adopting IFRS 16 in equity through retained earnings (or the equity adjustment account related to convergence), calculated as the difference between the carrying amounts of the right-of-use asset and the lease liability. This alternative is widely used by preparers because the date of initial application of IFRS 16 often differs from the commencement date of lease contracts, resulting in differences between the asset and liability balances. These differences are recognized as an adjustment to equity. Alternative 3 is similar to Alternative 2, except that it does not reflect any difference between the right-of-use asset and the lease liability. Under this approach, the lease contracts are assumed to be measured as if the date of initial application of IFRS 16 January 1, 2019 were the commencement date of the leases. As a result, the right-of-use asset and the lease liability are recognized at equal amounts.

These alternatives highlight the importance of establishing different approaches to the first-time application of IFRS 16. According to Varón (2022), the IASB decided not to require a fully retrospective approach for all leases in IFRS 16 as would normally be required under IAS 8, Accounting Policies, Changes in Accounting Estimates and Errors because the costs of such an approach could be significant and would outweigh the benefits (Table 8).

Lease payment

This corresponds to the disbursement of the monthly lease payment made in accordance with the agreement.

Table 8

Payment Made as of December 31, 2019 – First Year of Lease Contract CTA 001

Concept |

Debit |

Credit |

Lease liability |

$ 41.165 |

|

Interest expense |

$ 558.835 |

|

Banks |

|

$ 600.000 |

Source: Own elaboration.

Depreciation of the right-of-use asset

This corresponds to the systematic allocation of the cost of the right-of-use asset on a monthly basis. Table 9 presents the depreciation of the right of-use asset for the first year of the lease, allocated to the value of the asset’s cost over its useful life.

Table 9

Depreciation of the right-of-use asset – first year of lease contract CTA 001

Concept |

Debit |

Credit |

Depreciation cost |

$ 201.111 |

|

Accumulated depreciation – right-of-use asset |

$ 201.111 |

|

Source: Own elaboration.

Step 5: accounting and tax reconciliation of the contracts

The tax treatment of leases is governed by Article 127-1 of the National Tax Code (Estatuto Tributario), under which contracts are classified into two categories: finance leases (leasing) and operating leases (Luna, 2017). Finance leases are defined as those whose purpose is the financed acquisition of an asset (National Tax Code, 2026). This distinction is essential for determining whether a contract should be classified as finance or operating (Figure 3).

Figure 3

Leases under the Colombian tax code (Article 127-1)

Source: Own elaboration.

The test provided by Article 127-1 of the Tax Code, as established by Peña (2021), is similar to the former IAS 17 lease accounting standard, with full alignment between Article 127-1 and the superseded IAS 17. This convergence between accounting and tax standards is known as the formal connection principle, regulated by Article 21-1 of the Tax Code and Article 4 of Law 1314 of 2009 (Corredor, 2019). Notably, the principles of IFRS 16 regarding the recognition of operating leases differ significantly from those established in the tax regulations. This divergence introduced by IFRS 16 creates a disconnect between accounting and tax treatment, giving rise to deferred taxes.

For tax purposes, finance leases are defined as those whose purpose is the financed acquisition of an asset. In contrast, under IFRS 16, contracts classified as operating leases for tax purposes may be recognized as finance leases for accounting purposes, with right-of-use assets and lease liabilities recorded on the balance sheet. IFRS 16 introduces a specific approach to reflect in the financial statements the rights and obligations arising from contracts involving high-value underlying assets with terms exceeding one year, regardless of whether they constitute a financed acquisition of the asset (Peña, 2021). The differences between the accounting and tax treatments of these assets and liabilities give rise to deferred taxes associated with each contract previously evaluated, as shown in Table 10.

Table 10

Impact in profit or loss – contract CTA 001 compared to tax cost

| Period |

Interest expense |

Depreciation cost |

Total IFRS 16 |

Tax cost (Art. 59 Tax Statute) |

Difference |

|---|---|---|---|---|---|

1/01/2019 |

$ - |

$ - |

$ - |

$ - |

$ - |

31/12/2019 |

$ 58.835 |

$ 201.111 |

$ 759.946 |

$ 600.000 |

$ 159.946 |

31/12/2054 |

$ 80.898 |

$ 201.111 |

$ 282.009 |

$ 600.000 |

-$ 317.991 |

31/12/2055 |

$ 41.913 |

$ 201.111 |

$ 243.024 |

$ 600.000 |

-$ 356.976 |

Total |

$ 14.758.889 |

$ 7.441.111 |

$ 22.200.000 |

$ 22.200.000 |

-$ 0 |

Source: Own elaboration.

The interest expense and depreciation cost figures are derived from Table 11, while the tax value corresponds to the amount agreed upon in 2019 in the lease contract, which is used as a deductible cost in the income tax return pursuant to Article 59 of the Tax Code. Although IFRS 16 separates the financial component from the lease cost, the total payments at the end of the contract remain unchanged at COP $22,200,000. This temporary difference reverses over time, such that, at the end of the period, both accounting and tax results are equivalent.

Table 11

Effect on the statement of financial position – lease liability and its tax value (Contract CTA 001)

Fiscal reconciliation of lease liability |

|||||

Period |

Lease liability |

Tax liability |

Difference |

Tax 30% |

Adjustment |

1/01/2019 |

$ 7.441.111 |

$ - |

$ 7.441.111 |

$ 2.232.333 |

$ 2.232.333 |

31/12/2019 |

$ 7.399.946 |

$ - |

$ 7.399.946 |

$ 2.219.984 |

-$ 12.350 |

31/12/2054 |

$ 558.087 |

$ - |

$ 558.087 |

$ 167.426 |

-$ 155.731 |

31/12/2055 |

$ 0 |

$ - |

$ 0 |

$ 0 |

-$ 167.426 |

Source: Own elaboration.

The difference between the carrying amount of the asset and its tax value generates a deferred tax liability on the statement of financial position, which is recorded on January 1, 2019. This liability will begin to be adjusted, decreasing year by year until it reaches zero, as the temporary difference reverses. These temporary differences were calculated using the liability method based on the statement of financial position in accordance with IAS 12, which, according to Naula et al. (2020), allows control authorities to obtain a better description of the recognition of deferred tax assets and liabilities (Table 12).

Table 12

Effect on the balance sheet – lease asset and its tax-declared value (Contract CTA 001)

Fiscal reconciliation |

|||||

Period |

Lease asset |

Tax asset |

Difference |

Tax 30% |

Adjustment |

1/01/2019 |

$ 7.441.111 |

$ - |

$ 7.441.111 |

$ 2.232.333 |

$ 2.232.333 |

31/12/2019 |

$ 7.240.000 |

$ - |

$ 7.240.000 |

$ 2.172.000 |

-$ 60.333 |

31/12/2054 |

$ 201.111 |

$ - |

$ 201.111 |

$ 60.333 |

-$ 60.333 |

31/12/2055 |

-$ 0 |

$ - |

-$ 0 |

-$ 0 |

-$ 60.333 |

Own: Own elaboration.

The difference between the carrying amount of the liability and its tax value generates a deferred tax asset on the statement of financial position, which is recorded on January 1, 2019 (Table 13).

Table 13

Deferred tax accounting – assets and liabilities treated as a single transaction

| Period |

Deferred tax asset |

Deferred tax liability |

Asset-liability difference |

Annual Adjustment |

Entry |

|---|---|---|---|---|---|

1/01/2019 |

$ 2.232.333 |

$ 2.232.333 |

$ - |

$ - |

|

31/12/2019 |

$ 2.219.984 |

$ 2.172.000 |

$ 47.984 |

$ 47.984 |

Deferred tax asset |

31/12/2054 |

$ 167.426 |

$ 60.333 |

$ 107.093 |

-$ 95.397 |

Deferred tax asset |

31/12/2055 |

-$ 0 |

-$ 0 |

-$ 0 |

-$ 107.093 |

Deferred tax asset |

|

|

|

|

|

|

Source: Own elaboration.

On January 1, 2019, the deferred tax to be recognized is zero, since the calculation of the asset and liability results in the same amount, and compensating the two values produces a net effect of zero. At the close of 2019, a deferred tax does arise, given that the consumption of the asset follows a straight-line depreciation pattern while the consumption of the liability follows an amortized cost pattern, creating differences in the carrying amounts of the right-of-use asset and the lease liability. The tax value of both the asset and the liability is zero. Since this is a single transaction giving rise to both deferred tax assets and liabilities, it is recorded on a net basis. A transaction that is not a business combination for example, IFRS 16 leases may lead to the initial recognition of an asset or liability without affecting either accounting profit or taxable profit at the time of the transaction (IASB, 2016). The entity must apply the temporary difference approach and recognize any resulting deferred tax assets and liabilities when variations arise subsequent to initial recognition (Ministerio de Comercio, Industria y Turismo, 2022).

Step 6: analysis of additional considerations (Cash flows and EBITDA)

Under IAS 7, Statement of Cash Flows, the acquisition of a long-term asset through a finance lease contract is recognized as a non-cash item, since the initial measurement of the contract gives rise to a fixed asset and a financial liability element that do not affect cash flows at that moment. According to Peña (2021), this consideration can be applied to the measurement of right-of-use assets and lease liabilities, given that, at the time of initial recognition, there is no movement of cash or cash equivalents, only the recognition and measurement of an economic event. In the subsequent measurement, the lease liability is amortized in accordance with the lease payment made, with a direct charge to cash. In the authors' view, this effect is considered an item of operating cash flow, given the nature of the underlying economic event. It should be noted that the new requirements of IFRS 16 include the recognition of long-term liabilities that are not financed acquisitions of assets; for tax purposes, this applies only to the financial statements (Corredor, 2020).

In accordance with IAS 7, cash flows are classified as investing activities when they arise from the acquisition of fixed assets that are consumed over time (Calle & Figueredo, 2018). Depreciation of these assets is considered a non-cash item, regardless of whether the direct or indirect method is used. As for financing cash flows, these are affected by the incorporation of the liability and the effect of each of its payments (Barral et al., 2014). In the authors' view, interest expense could be considered an operating cash flow in the case of leases involving items of property, plant, and equipment.

With regard to the financial analysis of the contracts, the measurement of assets and liabilities for operating leases under IFRS 16 significantly impacts EBITDA, as its calculation starts from EBIT to which depreciation and amortization are added. The latter includes the consumption of the right-of-use asset recognized on the balance sheet. Previously, operating leases were recorded solely as a monthly operating expense.

According to PWC (2018), under the former standard, operating lease contracts were recognized directly in profit or loss as a line item of operating expenses. IFRS 16, by increasing the liability, generates variations in leverage ratios for example, net debt/EBITDA which is relevant in the evaluation of covenants and requires management to address this in the financial disclosures (Guijarro & Cortés, 2019). Other affected metrics include ROA, which may show significant variations, while ROE tends to show a more limited effect (Lopes & Penela, 2025). This is explained by the fact that the primary impact is reflected in the increase in total assets, directly affecting profitability. It is therefore recommended to calculate ROA with and without the effect of IFRS 16 for a more accurate analysis.

IFRS 7 requires entities to disclose information enabling users to understand the nature and extent of risks arising from financial instruments (Moreno, 2020). Among such instruments are lease liabilities measured at amortized cost; the indebtedness they generate forms part of the liquidity risk analysis, arising from non-cancellable contractual commitments. Leases thus represent a new fundamental element in the assessment of financial risk. Studies conducted before the implementation of IFRS 16 and following its issuance indicate that the sectors most significantly affected by the standard are hotels, retail trade, transportation, airlines, and bars and restaurants (Oliveira & Pettenuzzo, 2024). Future research should evaluate the post-implementation effects on companies in these sectors in Colombia.

Discussions

IFRS 16 significantly impacts traditional financial analysis by recognizing the financial cost of long-term contracts and incorporating right-of-use assets. In the case of Energías Limpias Sociedad BIC, the standard requires the recognition of liabilities that previously did not appear on the statement of financial position: for example, Contract CTA 001 gives rise to a liability of COP $7,441,111 that was not previously reflected in the entity's financing structure.

One of the most critical challenges in implementing the standard is the determination of the incremental discount rate. In this case, the absence of an implicit rate led to the use of the weighted average cost of existing financial obligations (7.51% EA). Although this approach is pragmatic and justified, it presents some ambiguity, particularly in long-term contracts where small variations in the rate can generate material differences in the value of the liability.

In terms of financial indicators, the incorporation of the right-of-use asset increases total assets and reduces ROA, without this reflecting a real deterioration in operating profitability. Likewise, the substitution of the straight-line lease expense with depreciation and interest raises EBITDA. The increase in the liability also affects leverage ratios, which may compromise covenants; this effect requires active and transparent management by the entity's leadership in the financial disclosures.

From a tax perspective, the disconnect between IFRS 16 and Article 127-1 of the Tax Code generates temporary differences from the first day of adoption, giving rise to net deferred taxes, since the right-of-use asset and the lease liability originate from the same transaction.

At the macroeconomic level, the application of IFRS 16 makes it difficult to compare results between Group 1 companies which apply full IFRS and Group 2 companies which apply the IFRS for SMEs since the latter does not contemplate the long-term lease accounting standard, which may affect comparability over time.

Conclusions

This case study synthesizes the correct application of IFRS 16 into six sequential steps. To facilitate its adoption, a thorough validation of lease contracts is essential, focusing on the identification of underlying assets, since a lease contract differs from a service agreement. The standard's test centers on determining whether the underlying asset is material in nature or has specific relative importance, which poses a challenge for the preparer, as estimating materiality involves value judgments. The materiality threshold is compared with the fair value of the asset; another relevant criterion is that the contract term, including possible renewals as defined by management, must exceed twelve months.

The discount rate applied to lease payments must be consistent with the term of the contract and the nature of the asset to be financed a critical point, particularly in agreements that do not involve the financed acquisition of the asset. The calculation of the contracts gives rise to the recognition of right-of-use assets and lease liabilities, as the agreement meets the definition of a present obligation. The implementation of these new valuations impacts income taxes by generating temporary differences and the corresponding deferred taxes, and modifies financial analysis in indicators such as EBITDA, leverage, and return on assets, among others.

As avenues for future research, it is recommended to evaluate the impact of the standard in sectors with higher volumes of operating leases, such as retail, commerce, industrial, logistics, and financial services. It is also relevant to examine aspects such as the revaluation of liabilities and assets due to changes in future lease payments; contract modifications; adjustments in tax rates for deferred tax calculations; reconciliations and disclosures in the notes to the financial statements; changes in decommissioning costs; the construction of discount rates; the presentation of right-of-use assets and liabilities in the statement of cash flows; and the effects on financial ratios.

Although this work is primarily applied in nature, its contribution to knowledge lies in the systematization of the IFRS 16 adoption process into six sequential steps, with a level of accounting, tax, and financial detail that is both novel and comprehensive, intended to contribute to the Spanish-language literature, particularly in the Colombian context. The purposive selection of the case ensures methodological rigor. The distinction between a didactic case and a scientific case study lies in the theoretical grounding, the systematization of the process, and the generation of conclusions that are transferable to other contexts criteria that this article fully meets.

Ethical Considerations

This research did not require ethics approval, as it was based on documentary review.

Conflict of interest

All authors declare that there is no conflict of interest related to this article.

Author contribution statement

Mario Andrés Peña Duarte: Writing – Original Draft. Formal Analysis, Validation, Research.

Ricardo Jesús Guerrero Díaz: Conceptualization; Methodology, Formal Analysis.

Miguel Antonio Piñerez Flórez: Writing: Review & Editing. Visualization.

Source of funding

This article was funded with the author’s own resources.

References

(1)Alzate, E. M. (2019). Aplicación de la NIIF 16. Identificación de un arrendamiento. Revista Internacional Legis de Contabilidad y Auditoría, (27). https://republicana.redbiblio.net/bib/15095

(2)Ariza, J. y Peña, M. A. (2023). Restructuración de pasivos financieros bajo NIFF en condiciones de crisis. Aglala, 14(1), 32-50. https://revistas.curn.edu.co/index.php/aglala/article/view/2248

(3)Armijo, F. L. (2019). NIIF 15 & NIIF 16. Teoría explicada con práctica. Autoedición.

(4)Barral, A., Bautista, R., Molina, H. D. y Ramírez, J. N. (2014). Marco conceptual del IASB y el debate a la norma de arrendamientos. Revista Internacional Legis de Contabilidad & Auditoría, (60), 57-82. http://hdl.handle.net/20.500.12412/1934

(5)Calle, R. y Figueredo, I. A. (2018). NIIF 16 Arrendamientos y la evaluación del impacto financiero y tributario en las empresas del sector construcción de Lima, Perú [Tesis de pregrado, Universidad Peruana de Ciencias Aplicadas]. Repositorio Académico UPC. https://doi.org/10.19083/tesis/624840

(6)Callo, K. S., Cortez, P. C., Pintado, D. E. & Salazar, J. (2025). NIIF 16 y la valorización de las empresas bajo los métodos de valorización: Flujo de caja descontado, múltiplo EBITDA y valor presente ajustado [Tesis de maestría, Universidad ESAN]. https://repositorio.esan.edu.pe/server/api/core/bitstreams/3d7c053b-8ba2-48b0-93b6-9e3aff3d92ba/content

(7)Carrillo, N. V. (2013). Normas Internacionales de Información Financiera (NIIF - IFRS). https://acortar.link/kYd9rc

(8) Christensen, D. M., Linsmeier, T. J. & Wangerin, D. D. (2025). Do reporting incentives and consequences change under the new lease accounting standard? The Accounting Review, 100(3), 159–185. https://doi.org/10.2308/TAR-2022-0266

(9)Código Civil. (s.f.). Artículo 1973 Definición de arrendamiento, https://leyes.co/codigo_civil/1973.htm#:~:text=Art%C3%ADculo%201973.,o%20servicio%20un%20precio%20determinado

(10)Corredor, O. (2019). Lecciones cortas de derecho tributario. Hache. https://editoreshache.com/producto/lecciones-cortas-de-derecho-tributario-2019-impreso/

(11)Corredor, O. (2020). El impuesto de renta en Colombia. Hache. https://editoreshache.com/producto/el-impuesto-de-renta-en-colombia-regimen-de-personas-naturales-app-rentas-naturales/

(12)Cueva, M., Cutipa, L. K., Ramírez, O. M., Mendoza, S. O. y Roque, D. (2025). Transformaciones contables de los arrendamientos operativos en el sector minero tras la adopción de la NIIF 16. Revista Científica Integración, 9(1), 43-50. https://revistas.uandina.edu.pe/index.php/integracion/article/view/908

(13)Delgado, D., Morales, J. & Zamora, C. (2022). IFRS 16 incremental borrowing rate: comparability issues and a methodology proposal for loss given default adjustment. Accounting in Europe, 19(2), 287–310. https://doi.org/10.1080/17449480.2022.2046282

(14)Delgado, D., Morales, J. y Zamora, C. (2023). Una propuestamodelo para el ajuste del IBR de la NIIF 16 basadoen la fijación de precios del mercado de bonos. Economic Research-EkonomskaIstraživanja , Taylor & Francis Journals, 36(2), https://ideas.repec.org/a/taf/reroxx/v36y2023i2p2106273.html

(15)Díaz, E. J. (2018). Incidencia de los arrendamientos mercantiles basados en el nuevo enfoque de la NIIF 16 – Arrendamientos aplicables en la empresa Brynajom S.R.L. de la ciudad de Huancayo-Junín [Tesis de pregrado, Universidad Peruana Los Andes]. Repositorio Institucional UPLA. https://repositorio.upla.edu.pe/bitstream/handle/20.500.12848/694/T037_71500080_T.pdf?sequence=1&isAllowed=y

(16)Estatuto tributario Nacional. (2026). Art. 127 - 1. Contratos de Leasing. https://estatuto.co/?e=1147

(17)Guijarro, P. y Cortés, A. (2019). Impacto de la NIIF 16 de contabilización de alquileres. Cuadernos de Información Económica, 268, 47–54. https://dialnet.unirioja.es/servlet/articulo?codigo=6780190

(18)IFRS. (2018). El Marco conceptual para la Información Financiera. https://www.mef.gob.pe/contenidos/conta_publ/con_nor_co/no_oficializ/ES_GVT_RedBV2016_conceptual.pdf

(19)International Accounting Standards Board. (2016). Norma Internacional de Información Financiera 16: Arrendamientos. IFRS Foundation. https://www.ifrs.org/content/dam/ifrs/publications/amendments/spanish/2016/niif-16-arrendamientos.pdf

(20)Lev, B. (2017). El final de la Contabilidad. Profif. https://es.scribd.com/document/605624713/El-Final-de-La-Contabilidad

(21)Lopes, A. I. & Penela, D. (2025). The impact of IFRS 16 on lessees' financial information: A single-industry study. Advances in accounting, 68, 100803. https://doi.org/10.1016/j.adiac.2024.100803

(22)Luna, Y. B. (2017). Revisoría fiscal ejercida con normas internacionales de auditoría y aseguramiento. ECOE Ediciones. https://www.ecoeediciones.com/wp-content/uploads/2017/08/Revisoria-fiscal-ejercida-con-normas-internacionales-de-auditoria-y-aseguramiento-1ra-Ed-.pdf

(23)Martinez, J. (2018). Contabilidad de los arrendamientos. USA: JCGtesting-com. https://www.amazon.com/-/es/Jose-D-Martinez-ebook/dp/B07J5VKHLM

(24)Ministerio de Comercio, Industria y Turismo. (2022). Decreto 1611 de 2022. https://www.mincit.gov.co/getattachment/cc94a98d-2e23-442c-8d09-53a9b3955675/Decreto-1611-del-5-de-agosto-de-2022.aspx

(25)Molina, H. y de Vicente, M. (2020). Análisis sobre los principales impactos de la hipotética aplicación de los criterios de la NIIF 16. “Arrendamientos” en cuentas individuales. AECA: Revista de la Asociación Española de Contabilidad y Administración de Empresas, 129, 5–9. https://aeca.es/wp-content/uploads/2020/05/revistaeca129_niif16_molina_devicente.pdf

(26)Molina, H., Vicente, M. y Ortiz, M. (2025). Interpretación del concepto de pasivo en la contabilidad de arrendamientos: Interpretation of the concept of liabilities in lease accounting. Revista De Contabilidad - Spanish Accounting Review, 28(1), 57–70. https://doi.org/10.6018/rcsar.538161

(27)Mora, A. (2021). Contabilidad Financiera Analisis y supuestos practicos. Navarra: Thomson Reuters Proview. https://books.google.com.co/books/about/Contabilidad_financiera.html?id=7aBBEAAAQBAJ&redir_esc=y

(28)Morales, J. y Zamora, C. (2018). Implementación de la NIIF 16 (arrendamientos): impacto de las decisiones de la empresa en los estados financieros. https://idus.us.es/items/f32b17cd-07f2-4791-bdfe-2986333a047f

(29)Moreno, J. (2020). Análisis de un caso de estudio en Colombia en instrumentos. Fundación lasirc, 1(16), 8-22. https://drive.google.com/file/d/1bmERfA-CZGDdg7AWrsLRzeoQhIgm4_bD/view

(30)Moscariello, N. & Pizzo, M. (2022). Practical expedients and theoretical flaws: the IASB's legitimacy strategy during the COVID-19 pandemic. Accounting, Auditing & Accountability Journal, 35(1), 158-168. https://doi.org/10.1108/AAAJ-08-2020-4876

(31)Naula, F. B., Arévalo, D. J., Campoverde, J. A. y López, J. P. (2020). Estrés financiero en el sector manufacturero de Ecuador. Revista Finanzas Y Política Económica, 12(2), 461–490. https://doi.org/10.14718/revfinanzpolitecon.v12.n2.2020.3394

(32)Oliveira, W. & Pettenuzzo, P. (2024). A IFRS 16 sob a perspectiva da True and Fair View. Revista De Gestão E Secretariado, 15(10), e4282. https://doi.org/10.7769/gesec.v15i10.4282

(33)Orozco, J. D. (2015). Valoracion de Instrumentos Financieros en NIIF para pymes. Ecoe. https://books.google.com.co/books?hl=es&lr=&id=GTSjDwAAQBAJ&oi=fnd&pg=PA5&dq=related:P2DAKd194VEJ:scholar.google.com/&ots=vWrQ_OtBS_&sig=pAB34n0mEDPi-zf7xZ3-9W7s-_s&redir_esc=y#v=onepage&q&f=false

(34)Peña, M. A. (2021). Los efectos en la información financiera que generan el reconocimiento, medición y revelación de instrumentos financieros, bajo los requerimientos de las Normas Internacionales de Información Financiera aplicadas en Colombia [Tesis de maestría, Universidad de Santander]. Repositorio Institucional UDES. https://repositorio.udes.edu.co/handle/001/5458

(35)PWC. (2018). highlight report. https://www.pwc.pe/es/publicaciones/Highlights/agosto-2018.pdf

(36)Ramírez, B. V. (2017). La NIIF 16: Una Norma Contable que llega tras 30 años de la NIC 17. Revista Internacional Legis de Contabilidad y Auditoría, (69), 27-70. https://xperta.legis.co/visor/rcontador/rcontador_928457e0fc2a48be9dfab5ac6b61c2f3

(37)Ramirez, J. C. (2019). Aplicación de la NIIF 16 Arrendamientos en el sector aeronáutico. Revista Internacional Legis de Contabilidad y Auditoría, (78), 129-146. https://ru.dgb.unam.mx/items/13e0ad2a-e410-4607-9832-911e2c2f3f1d

(38)Rojas, L. K. & Franco, Y. A. (2022). Effects of implementation ifrs 16 in colombian companies listed on the colombian stock exchange. Revista Facultad de Ciencias Económicas: Investigación y Reflexión, 30(2), 43–58. http://www.scielo.org.co/scielo.php?pid=S0121-68052022000200043&script=sci_arttext

(39)Romero, M. (2021). Enmiendas a la NIIF 16 por COVID 19 Aplicación Práctica. Revista Internacional Legis de Contabilidad y Auditoría, (85), 11-26. https://xperta.legis.co/visor/rcontador/rcontador_bc7538f980ad4d058ef68e5391cc939a

(40)Salazar B., Salazar B. y Marín S, (2015). Contabilidad financiera para pequeñas y medianas empresas: Guía de aplicación práctica para las entidades del grupo 2 (2.ª ed.). Legis. https://www.legis.com.co/contabilidad-financiera-para-pymes/p?srsltid=AfmBOoquByoikT2CBXI-MO88yqJORqjNpQwGXHaQ16KOqA44fX99rvoC

(41)Tejada, Á., Pérez, R., Ramírez, Y., González, R., Sánchez, M. P., Tejedo, F., Báidez, A., González, J., Moreno, J. L. y Pontones, C. (2017). Manual práctico de contabilidad. Ediciones Pirámide. https://www.edicionespiramide.es/libro/economia-y-empresa/manual-practico-de-contabilidad-angel-tejada-ponce-9788436838206/

(42)Varón, L. (2022). Efectos de la NIIF 16 Arrendamientos en empresas que cotizan en el mercado de valores colombiano. Revista internacional legis de contabilidad y auditoría, (89), 77-94. https://xperta.legis.co/visor/rcontador/rcontador_873f871b9fa947629126170b1e24724e

(43)Varón, L. (2023). ¿Qué se discute en el Proyecto de Norma “Tercera edición de la NIIF para las pymes”? https://xperta.legis.co/visor/rcontador/rcontador_CONTENIDO_ULTIMA_ACTUALIZACION