Finance

Boar of directors and value of Chilean companies

Consejo de administración y valor de empresas chilenas

Conselho de administração e valor das empresas chilenas

Por: 1 Felipe Muñoz Chávez![]() ;2 Andrea King Domínguez

;2 Andrea King Domínguez![]() ; 3 Rosa Martha Ortega Martínez

; 3 Rosa Martha Ortega Martínez![]()

![]()

1Master’s in Business Management, University of Bío-Bío, Chile. Researcher, Department of Business Management, University of Bío-Bío. ORCID: 0009-0007-5046-3694. E-mail: felipe.munoz1801@alumnos.ubiobio.cl. Chillán - Chile.

2PhD in Business Administration, Polytechnic University of Catalonia, Spain. Academic, Department of Economics and Finance, University of Bío-Bío. ORCID: 0000-0002-1063-4336. E-mail: aking@ubiobio.cl. Concepción - Chile.

3Master’s in Finance, Juárez University of the State of Durango, Mexico. Academic, Faculty of Economics, Accounting and Administration, Juárez University of the State of Durango (UJED). ORCID: 0000-0003-0940-723X. E-mail: rmortega@ujed.mx. Durango - Mexico.

4PhD in Business Administration, Polytechnic University of Catalonia, Spain. Academic, Department of Business Management, University of Bío-Bío. ORCID: 0000-0003-0482-0287. E-mail: lamestica@ubiobio.cl. Chillán - Chile.

DOI: https://doi.org/10.22267/rtend.252601.265

How to cite this article: Muñoz, F., King, A., Ortega, R. & Améstica, L. (2025). Board of directors and value of Chilean companies. Tendencias, 26(1), 61-88. https://doi.org/10.22267/rtend.252601.265

![]()

Abstract

Keywords: Chile; board of directors; economic evaluation; finance; corporate governance.

JEL: G30; G32; G34; M21.

Resumen

Palabras clave: Chile; directorio; evaluación económica; finanzas; gobierno corporativo.

JEL: G30; G32; G34; M21.

Palavras-chave: Chile, conselho de administração; avaliação econômica; finanças; governança corporativa.

JEL: G30; G32; G34; M21.

Introduction

The ability to estimate the value of companies is increasingly relevant, both for investors and owners themselves, as it directly affects their investment and profit. This responsibility lies with the Board of Directors (BoD), also referred to as the board or governing body in other regions. The relationship between the performance of these boards and their composition is an increasingly studied topic, based on the premise that performance results from the responsibility and contribution of its board members. It is crucial to understand the characteristics of these boards that enable efficient and effective decision-making for the favorable development of the company.In general, research in this area has shown that studies do not always reach the same conclusion. This difference may be due to various estimation methods used, different countries, and different study periods (Campbell & Mínguez, 2008). It is worth noting that this type of research is primarily approached quantitatively with longitudinal studies, examining the characteristics of the BoD over time and their effect on profitability or value creation in the company.It is important to highlight that in Latin America, there are few studies explaining the impact of BoD characteristics on value creation, which is why this research helps bridge that information gap for the case of Chile, in contrast to studies conducted in developed economies (King et al., 2018).

The companies under study are listed on the stock exchange through the Índice General de Precios de Acciones [General Stock Price Index] (IGPA) and are entirely public limited companies, in accordance with Chilean regulations. Regarding the BoD, there are no specific requirements for its composition, but it is mandated to report the characteristics of its members, which aims to, among other things, reduce the gender gap. On the other hand, public companies and those related to the Chilean state, according to current regulations, must ensure that no single gender has more than 60% representation on the board. This would pressure public limited companies in the future to establish some gender quota to increase female participation, with the draft law “Más Mujeres en Directorios [More Women on Boards]” (Ministerio de Economía, 2024).

Decision-making is the key factor determining whether many activities in companies are successful or fail. For this reason, certain characteristics are valued for executive positions to make the best decisions for the organization. Thus, some characteristics become key resources (Cruzat et al., 2021).

Despite the numerous studies and research conducted over time, it is still difficult to definitively conclude the effect of BoD member characteristics on company performance, and more specifically on company value or stock value (Lakatos, 2020).

Boards of Directors in Companies

The Organisation for Economic Co-operation and Development (OECD) highlighted the importance of good Corporate Governance (CG) in every company in 2016, defining it as an entity that ensures equitable treatment for all shareholders. It is also conceived as a system that creates an appropriate environment for the power relations between the company’s management, the Board of Directors (BoD), shareholders, and other stakeholders, serving as a fundamental promoter of financial stability and integrity within the company and its business (OECD, 2016).

BoDs constitute one of the main mechanisms of internal CG, acting on behalf of the shareholders and being considered a relevant body in decision-making within the company, assuming the role of intermediary between shareholders and top management (Merendino & Melville, 2019). Its supervisory function is a control instrument of CG that aligns the interests of management, the board, controlling shareholders, minority shareholders, and other stakeholders (Campbell & Mínguez, 2008).

Agency relationships within an organization are established when one or more people appoint another, called an agent, to represent them, and the latter acts with delegated authority in decision-making. It is imperative for the BoD to oversee the agent’s actions. However, there is evidence that the agent does not necessarily act in the interest of the principal, giving rise to the so-called agency conflicts. In this context, it is essential for the principal to limit deviations from the mandate by establishing proper incentives for the agent and incurring supervision costs. Therefore, this supervisory role played by BoDs could mitigate the agency problem between shareholders and management (Jensen & Meckling, 1976).

Thus, the problem of how a good BoD should be composed arises. Campbell & Mínguez (2008) assert that the effectiveness of the BoD as a supervisor depends on the qualifications or characteristics of its members.

Characteristics of Boards of Directors

The composition of BoDs is one of the most researched topics in corporate governance (CG) studies, as this composition affects the decision-making processes of the board, the way it performs its functions and roles, the board’s effectiveness, and consequently, the financial outcomes of the company (Pavić et al., 2018).

Establishing a clear relationship between certain characteristics of BoDs and an estimation of their economic value as a company remains a challenge. Research conducted to analyze this relationship has identified more common characteristics, such as the size of the BoD based on the number of members, female participation in boards, or the professional diversity of those who participate in the boards (Améstica et al., 2021).

Board Size

In the literature, the influence of size, understood as the number of people participating in BoDs, on company performance is still unclear. However, multiple studies on the topic and ideas proposed by their authors can be found.

One line of research argues that a larger BoD could improve the efficiency of the decision-making process due to the exchange of information. This is observed in a study conducted on companies with a high degree of survival, as shown in Lehn et al.'s (2009) report, which covers U.S. companies from 1935 to 2000, working with panel data over time periods. This line of research also asserts that a larger BoD may have greater potential among its members, justified by the greater heterogeneity in knowledge, experience, and values of its members, which is related to the financial results of board members of companies in the Spanish industry (Barroso et al., 2010).

The positive relationship between BoD size and the economic value of the company is confirmed in Pucheta's (2015) study, where he concluded that larger boards positively impact the company’s value, resulting in greater wealth for shareholders. However, this increase in company value is limited to a certain point, as adding another member beyond this point may negatively affect the company's value.

On the other hand, Treepongkaruna et al. (2024) suggest that companies with larger boards tend to face fewer environmental, social, and governance-related controversies. These findings are grounded in resource dependency theory, indicating that larger boards are generally more effective, and in stakeholder theory, which promotes corporate sustainability and avoids controversial activities.

Conversely, Ahmed et al. (2006) suggest that a larger BoD is less effective at improving company performance because it is less likely to express new ideas and opinions. Moreover, the supervision and control process is affected. Similarly, Merendino & Melville (2019) note that BoD size has a positive effect on company outcomes, especially when the board is smaller.

Bonn et al. (2004) present the case of Japanese companies, where BoD size was negatively associated with both the Market to Book ratio and ROA. This finding supports the claim that large boards are less cohesive, more difficult to coordinate, and tend to be less involved in strategic decision-making. Furthermore, Lakatos (2020), in a study of publicly listed non-financial companies in Central and Eastern Europe, concluded that there is a negative relationship between board size and company value. Therefore, increasing the company size does not necessarily mean the BoD size should be increased.

Additionally, in Iberian companies, a larger BoD negatively affects Return on Assets (ROA) and Return on Equity (ROE), due to communication problems that may lead to poor decision-making, thus affecting the board’s effectiveness. The negative relationship is also confirmed in the case of the Market to Book ratio, indicating that older directors are beneficial, as their experience grants them better management skills (Proença & Neves, 2022).

In the research conducted by Torres and Correa (2021) on the impact of CG practices on the value of companies in the Mercado Integrado Latinoamericano [Latin American Integrated Market], it was determined that good CG practices, such as controlling board size, have a positive outcome on economic value.

A study conducted in Chile by King et al. (2018) found that BoD size positively affects financial ratios like ROA and sales margin, but only up to a certain point. This is because the optimal number of directors must be respected; otherwise, the relationship would turn negative.

Women’s Participation in the Board of Directors

Women’s participation in Boards of Directors (BoDs) is studied as a factor related to the number of female members in relation to the total number of participants. The aim is to determine whether the inclusion of women in BoDs contributes to company performance.

Gender diversity, in particular, is an intriguing issue that has gained even more importance due to changes in the labor market over the past two decades and the increase in participation and legal mandates for the inclusion of women in boards of directors (Pavić et al., 2018).

According to Pucheta (2015), women's participation has a positive effect on BoDs, contributing to the creation of business value. This is explained by the different perspectives and diversity of opinions offered by female directors, leading to more democratic decisions and improving the decision-making process. Similarly, Campbell & Mínguez (2008) confirm this relationship for Spanish companies, noting that gender diversity positively impacts company value, meaning that greater gender diversity can generate economic benefits.

In line with this, Erhardt et al. (2003) argue that, in the case of large U.S. companies, the percentage of women is positively associated with stock performance and investment return, as the supervisory role can be effective when conflicts arise, allowing for a broader range of opinions to address associated problems. Likewise, Fernández et al. (2024) state that a higher number of women in BoDs affects the cost of debt by reducing it. The inclusion of at least one woman as a director has been shown to lower the cost of credit compared to exclusively male boards. Furthermore, the effect of a lower loan spread is stronger with the inclusion of the first woman and weakens with each additional female director.

A higher female presence in BoDs has improved financial performance ratios such as ROA and ROE, but only up to a certain point. This is because the mandatory inclusion of more women in the boards, imposed by legal requirements, has led to decreased financial returns. It is estimated that with a 20% gender quota, a maximum market value is achieved (Proença & Neves, 2022). Similarly, Campbell & Mínguez (2008) note that the presence of women in BoDs could increase shareholder value, provided that women contribute an additional perspective to the board's decision-making. However, if the decision to include women on the board is driven by social pressure for greater gender equality, it could negatively impact company outcomes.

Smith et al. (2006), in their study of Danish companies, argue that a BoD with greater gender diversity can increase a company's competitive advantage, if it improves the company’s image and has a positive effect on customer behavior, thereby improving company results. However, they did not find a significant relationship between female representation on BoDs and company performance. Similarly, Salehi & Zimon (2021) indicate that there is no substantial evidence linking gender diversity with the creation of economic value, suggesting that the appointment of female directors does not depend on company growth and performance, and that external factors such as the company's competitive position have a greater impact on economic results.

In contrast, Jianakoplos & Bernasek (1998) associate women on BoDs with lower financial performance in companies, due to their higher aversion to risk. This was the result of their study examining gender differences in household asset ownership. The study found a reduction in the proportion of risky assets when dealing with single women, and this trend increased with the number of children in the household. In another article reviewing research arguments and data on how diversity management generates a competitive advantage, it was found that the presence of more women in the company increases costs due to higher turnover and absenteeism among them (Cox & Blake, 1991). Continuing with this stance, Pavić et al. (2018) investigated Croatian insurance companies and inferred that the mere presence of women on the board does not automatically improve companies' financial performance, and that promoting gender diversity on BoDs could negatively affect performance.

Bøhren & Strøm (2007) found a significantly negative relationship between the proportion of women on BoDs and profitability in Norwegian companies. According to their study, heterogeneous boards are less effective in decision-making.

Regarding gender diversity, Verona and Fuertes (2020) note that women’s participation in senior management and BoDs in Spain is still relatively low, averaging 18.22% on BoDs in 2017. Although there has been an upward trend during the study period, they affirm that female participation remains far from the recommendations of Spanish regulations, resulting in underrepresentation in both bodies.

Studies conducted in Latin America report low female participation in boards of directors. In a study on companies in Brazil, Chile, and Mexico, no evidence was found that greater female participation improves financial performance (Arévalo et al., 2020). In Mexico, a negative relationship was found between the participation of a woman on the BoD and ROA, with the same relationship when the participation consists of three women. However, the study notes that the participation of female directors has been increasing following suggestions from the Mexican Stock Exchange, though participation remains low, and these results may be symbolic when analyzed with the Generalized Method of Moments (GMM) approach, explaining that low participation may lead to an overestimation of results based on the methodology used, suggesting caution in interpreting the results (Rosas et al., 2023).

It is important to highlight that, in the case of Chile, with the GMM model, measured through Tobin's Q, it can be inferred that female leadership has a negative social perception. Arenas et al. (2020) studied the composition of boards of directors in Chile regarding diversity. One of the variables investigated was gender, and it was found that female participation is low, with boards being composed, on average, of 7.70 directors, of which only 0.45 are women.

Professional Diversity of the Board of Directors

In the same context as the two previously mentioned variables—size and female participation in the boards of directors—the professional diversity of the board has varied results. Professional level is described as the level of academic education.

Simons & Pelled (1999) mention that demographic changes in the workforce, along with equal opportunity laws, mean that diversity is increasing in most workplaces, even in managerial and executive ranks. They suggest that cognitive and educational diversity has positive effects on an organization; however, they argue that diversity of experience is negatively associated with investment performance. They further contend that the benefits of educational diversity can be observed in organizational performance across different sectors and that it is not specific to any one industry.

Bantel (1993) suggests that better strategic decision-making is positively influenced by greater functional diversity and higher levels of education within top management teams. He also adds that the dynamics of connectivity affect the development of human capital within the financial networks of developing countries.

In a study conducted in Italian companies using a regression model, Romano & Guerrini (2014) found that the educational level of members influences economic performance, where graduate and senior directors exert a negative influence on profitability. Additionally, they considered that public companies are less profitable than private or mixed companies.

Meanwhile, Murray (1989) worked with a sample from the food and oil sectors of the Fortune 500 list, which included occupational and educational backgrounds as occupational heterogeneity, and concluded that it has little relevance to short-term company performance. He also found a negative relationship with long-term performance.

In Europe, studies on banks within the so-called Eurozone concluded a negative relationship between educational background and financial performance, explained by agency problems, as some board members may use their experiences and knowledge for their personal interests. They suggest more rigorous measures from the European Central Bank to control the behavior of board members (Pereira & Filipe, 2022).

In Indonesia, it was found that there is no relationship between educational background and the ROA indicator, based on the premise that managerial experience helps acquire greater knowledge and skills in executive roles. On the other hand, there is evidence of a positive relationship between educational background and market valuation according to Tobin's Q, where the market perceives that companies with highly educated boards achieve good performance. This is based on improvements in strategies that attract good investors and strengthen networks with stakeholders, such as governments, which are necessary for business operations (Darmadi, 2013).

Proença & Neves (2022) analyzed the relationship between board members’ qualifications and financial performance, measured by ROA and ROE, as well as market value. The results differ, as directors with lower qualifications have a positive effect on financial performance, explained by other variables such as age. From experience, they can add value to company results. In contrast, directors without postgraduate studies negatively affect the Market to Book ratio, suggesting that greater specialization improves market valuation by potential investors.

Salehi & Zimon (2021) argue that there is no significant relationship between the educational diversity of board members and value creation or growth within companies. However, these results may be conditioned by the exclusion of important variables in Iranian business performance, such as director characteristics, ownership structure, and auditor characteristics.

In Brazil, there are diversified boards, although there is no evidence that this impacts financial performance, as the results show low statistical significance. The study highlights that 49.6% of directors have master's or doctoral degrees, and the most common professions in the boards are in the areas of Engineering, Management, Economics, and Law (Cruzat et al., 2021).

Based on the above, the study proposes the following hypotheses:

H1: There is a positive relationship between the size of boards of directors and the creation of economic value.

H2: The participation of women on the board of directors has a positive influence on the value of the company.

H3: Greater professional diversity in the board of directors has a positive impact on the creation of economic value.

Methodology

This research is explanatory and quantitative with a longitudinal approach. It analyzes the causality between the variables of the Board of Directors (Board size, female participation, and professional diversity) in the creation of economic value, applied to Chilean companies during the period 2019-2022.

The necessary information for constructing the set of variables related to the Board of Directors was obtained from the annual reports of the companies, the website of the Chilean Securities and Insurance Commission (Comisión para el Mercado Financiero), and the Economatica platform. Additionally, data from the Damodaran website was used to obtain a database of multiples for emerging markets, which were employed in calculating firm value.

Furthermore, the literature review, which complements the research through various approaches and methodologies that can be utilized, is based on secondary sources. Databases such as Web of Science, Scopus, and Google Scholar were consulted.

The initial sample for this study consists of the companies listed in the IGPA index of the Santiago Stock Exchange during the period 2019-2022. Subsequently, financial companies were excluded, as previous studies (Arévalo et al., 2020; Briano & Pucheta, 2015; Rodríguez, 2016) suggest excluding such companies due to their different accounting practices and higher debt ratios, which could lead to biases that alter the results.

In addition, as an exclusion criterion, only companies with at least one year of stock market participation were considered, excluding those without sufficient market presence. Data regarding their boards of directors and financial background was gathered. Based on the above, the study covered 51 companies in 2019, and 48 companies in subsequent years.

Variables

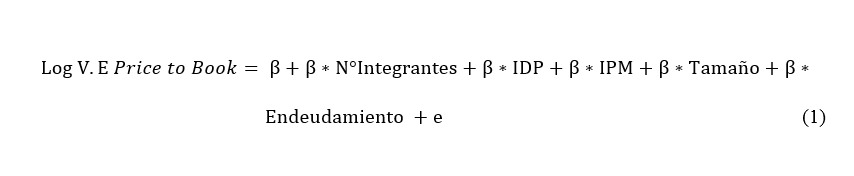

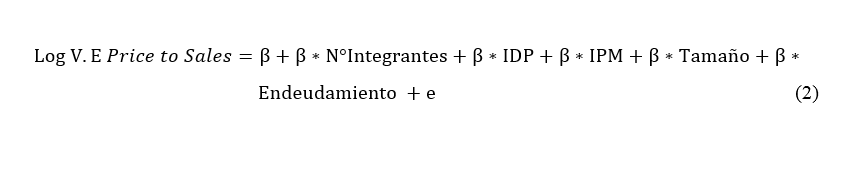

The dependent variable is the firm value, calculated using the multiples method from an emerging market perspective, considering that Chile fits this classification. Three approaches were used: Price to Book (Price/Book value by Industry Group), Price to Sales (Price/Sales ratio by Industry Group), and EV to EBITDA (Enterprise Value/EBITDA by Industry Group). The independent and control variables (see Table 1) are: the number of board members, the Female Participation Index (FPI), the Professional Diversity Index (PDI), and control variables such as company size and debt level.

Table 1

Independent and Control Variables

Variable |

Description |

Authors |

Independent |

||

Participants |

Total number of participants in the Board of Directors (BoD). |

Barroso et al. (2010), Lakatos (2020), Merendino & Melville (2019), Pucheta (2015). |

WPI |

Women Participation Index: ratio of the number of women to the total number of participants in the BoD. |

Arévalo et al. (2020), Briano & Rodríguez (2016), Campbell & Mínguez (2008), Pavić et al. (2018). |

PDI |

Professional Diversity Index: ratio of the number of different professions to the total number of participants in the BoD. |

Cruzat et al. (2021), Salehi & Zimon (2021). |

Control |

||

Size |

Company Size: measured by the natural logarithm of the company’s total assets. |

Briano & Rodríguez (2016), Campbell & Mínguez (2008), Pavić et al. (2018), Torres and Correa (2021). |

Leverage |

Leverage: measured by the fraction of total debt over total assets. |

Campbell & Mínguez (2008), King et al. (2018), Lakatos (2020), Pucheta (2015). |

Source: Prepared by the authors.

Methods and Analysis Techniques

First, an analysis of the composition of the BoDs of the companies in the sample was conducted, where the name, gender, and profession of each board member were collected. For professions, undergraduate studies from Universities or Educational Institutions were considered, as well as other professional activities. Methodologically, in cases where the profession was not explicitly stated or only postgraduate studies were mentioned, the profession was considered as “not reported,” although this occurred on rare occasions. Additionally, it should be noted that the profession "Ingeniero Comercial [Commercial Engineer]" (similar to Bachelor’s degrees in Administration and Economics in other countries) is a discipline in the field of economic and administrative sciences that is not present in all countries. Generally, it is referred to as "business administrator." At the same time, so-called entrepreneurs are individuals who do not hold an academic degree but have experience in the business world.

The data on the number of board members, PDI, and WPI for the total number of companies were analyzed using descriptive statistics for each period. In addition to the creation of tables that provide relevant information about the studied variables.

Next, a multiple linear regression was conducted, with companies categorized according to their industry classification from the Damodaran website, using the business valuation multiple corresponding to emerging markets, which is updated annually.

Subsequently, the company value was calculated using the three dependent variables mentioned earlier, in addition to the control variables included in the equation. It is important to note that the proposed regression models are independent of each other, using data collected from the four years of study.

Multiple Linear Regression Model

The information and results collected earlier were grouped into a panel data table for the four years of study. Statistical tests were conducted to make adjustments to the regression model. Due to issues of heteroscedasticity, the dependent variable for all regressions was modified, where the previously calculated company value was replaced by the natural logarithm of the firm value, yielding results for the regression models within acceptable ranges.

The regression Equations (1, 2, and 3) represent the natural logarithm of the company value for each multiple, as well as the natural logarithm of the average company value of the three previously described multiples (Price to Book, Price to Sales, and EV to EBITDA), both as dependent variables. In these equations, the number of members, WPI, PDI, company size, and debt act as independent variables.

Results

Composition of the Boards of Directors of Chilean Companies that Make Up the IGPA

The Chilean companies that were part of the study for at least one year amounted to 54. Below, Table 2 presents the main characteristics of the composition of the boards of directors for each year of study.

Table 2

Composition of the Boards of Directors of IGPA Companies

Statistic |

2019 |

2020 |

2021 |

2022 |

||||||||

N° |

WPI |

PDI |

N° |

WPI |

PDI |

N° |

WPI |

PDI |

N° |

WPI |

PDI |

|

Mean |

7.94 |

0.09 |

0.64 |

7.83 |

0.09 |

0.62 |

7.83 |

0.14 |

0.62 |

7.88 |

0.17 |

0.62 |

Median |

7 |

0.11 |

0.67 |

7 |

0.11 |

0.57 |

7 |

0.14 |

0.59 |

7 |

0.14 |

0.59 |

Mode |

7 |

0 |

0.57 |

7 |

0 |

0.57 |

7 |

0 |

0.71 |

7 |

0.14 |

0.71 |

Minimum |

5 |

0 |

0.33 |

5 |

0 |

0.29 |

5 |

0 |

0.22 |

5 |

0 |

0.30 |

Maximum |

14 |

0.33 |

1 |

14 |

0.33 |

1 |

14 |

0.43 |

0.86 |

14 |

0.6 |

0.89 |

Variance |

1.90 |

0.01 |

0.03 |

1.93 |

0.01 |

0.03 |

1.93 |

0.02 |

0.03 |

1.94 |

0.02 |

0.02 |

Standard Deviation |

1.38 |

0.10 |

0.16 |

1.39 |

0.11 |

0.16 |

1.39 |

0.12 |

0.16 |

1.39 |

0.13 |

0.15 |

Source: Prepared by the authors.

When reviewing the data chronologically, a trend is observed in the average number of board members, which remains close to 8 during the four years of study. The minimum number of members is 5, and the maximum is 14, with variance fluctuating between 1.9 and 1.94, and standard deviation between 1.38 and 1.39, indicating low dispersion. This is further confirmed by the fact that both the median and the mode are 7.

The WPI (Women Participation Index) is very low for the years 2019 and 2020, considering that women's participation in the board is only 9%. However, a considerable increase to 17% is observed in 2022. It is noteworthy that, in the first three years of study, the mode is 0, suggesting that the participation of women on the boards is absent in a significant number of the companies studied.

The PDI (Professional Diversity Index) varies between 0.64 and 0.62, indicating that professional diversity in Chile is moderately high. This is supported by the low variance and standard deviation of the data.

Regarding the size of the boards per year, Table 3 shows that the vast majority of non-financial companies listed on the IGPA have boards of 7 members, a figure that exceeds 52% during the four years of study, followed by 9 members. The concentration of these two sizes is noteworthy, as 43 of the 48 companies present between the years 2020 and 2022 have boards made up of 7 or 9 members.

Table 3

Board Size by Year

BoD Size |

2019 |

2020 |

2021 |

2022 |

||||

N° |

% |

N° |

% |

N° |

% |

N° |

% |

|

5 |

1 |

1,96% |

1 |

2,08% |

1 |

2,08% |

1 |

2,08% |

6 |

0 |

0% |

0 |

0,00% |

0 |

0,00% |

0 |

0,00% |

7 |

27 |

52,94% |

28 |

58,33% |

28 |

58,33% |

27 |

56,25% |

8 |

2 |

3,92% |

2 |

4,17% |

2 |

4,17% |

2 |

4,17% |

9 |

19 |

37,25% |

15 |

31,25% |

15 |

31,25% |

16 |

33,33% |

10 |

1 |

1,96% |

1 |

2,08% |

1 |

2,08% |

1 |

2,08% |

11 |

0 |

0% |

0 |

0% |

0 |

0% |

0 |

0% |

12 |

0 |

0% |

0 |

0% |

0 |

0% |

0 |

0% |

13 |

0 |

0% |

0 |

0% |

0 |

0% |

0 |

0% |

14 |

1 |

1,96% |

1 |

2,08% |

1 |

2,08% |

1 |

2,08% |

Total |

51 |

100% |

48 |

100% |

48 |

100% |

48 |

100% |

Source: Prepared by the authors.

As shown in Table 3, it should be considered that the variation between 2019 and 2020 is due to changes in the composition of the IGPA, as between 2020 and 2022 the same companies remained. Only in one case, in 2022, did a company increase its board size from 7 to 9 members.

When analyzing the number of women present on each of the boards (Table 4), it is evident that there is low participation, although there is a trend toward greater inclusion in recent years. In 2019, 45.1% of boards did not include women, a figure that decreased to 20.83% by 2022. Similarly, there is a progressive increase in boards with 2 or 3 women, especially in the latter case, wherein in 2022, 14.58% of boards had 3 female participants, a figure notably higher than the 1.96% observed in 2019.

Table 4

Women’s Participation in the Boards of Directors by Year

Women in BoD |

2019 |

2020 |

2021 |

2022 |

||||

N° |

% |

N° |

% |

N° |

% |

N° |

% |

|

0 |

23 |

45,10% |

22 |

45,83% |

16 |

33,33% |

10 |

20,83% |

1 |

20 |

39,22% |

19 |

39,58% |

17 |

35,42% |

18 |

37,50% |

2 |

7 |

13,73% |

4 |

8,33% |

11 |

22,92% |

13 |

27,08% |

3 |

1 |

1,96% |

3 |

6,25% |

4 |

8,33% |

7 |

14,58% |

Total |

51 |

100% |

48 |

100% |

48 |

100% |

48 |

100% |

Source: Prepared by the authors.

In Table 5, it can be seen that Commercial Engineers are the most frequent profession in the boards of directors during the study period, with a representation close to 33%, followed by Industrial Civil Engineers, Civil Engineers, and Lawyers, which have a representation ranging between 11.5% and 13.4%. The fifth most frequent profession is entrepreneurs. Together, the five professions mentioned above account for 74.53% of the total participants in the boards of directors.

Table 5

Most Relevant Professions in the Boards of Directors by Year

Profession |

N°2019 |

N°2020 |

N°2021 |

N°2022 |

N° 2019-2022 |

% |

|

|

|||||||

Commercial Engineer |

132 |

126 |

126 |

119 |

503 |

32,77% |

|

Industrial Civil Engineer |

52 |

53 |

52 |

49 |

206 |

13,42% |

|

Civil Engineer |

49 |

49 |

47 |

48 |

193 |

12,57% |

|

Lawyer |

43 |

42 |

44 |

48 |

177 |

11,53% |

|

Entrepreneur |

21 |

16 |

15 |

13 |

65 |

4,23% |

|

Total of 5 most frequent professions |

297 |

286 |

284 |

277 |

1144 |

74,53% |

|

Other professions |

108 |

90 |

92 |

101 |

391 |

25,47% |

|

Total board members |

405 |

376 |

376 |

378 |

1535 |

100% |

|

Source: Prepared by the authors.

Results of the Multiple Linear Regression Model

Table 6

Model Fit and Autocorrelation Tests

Model |

R |

R2 |

Adjusted R² |

Durbin-Watson |

Log Price to Book |

0,902 |

0,813 |

0,808 |

1,730 |

Log Price to Sales |

0,842 |

0,710 |

0,702 |

1,964 |

Log Ev to Ebitda |

0,876 |

0,767 |

0,761 |

1,927 |

Source: Prepared by the authors.

The regression results (Table 7) show that the number of members is significant at the 1% level and has a positive influence on firm value, moderately affecting the first dependent variable. Therefore, Hypothesis 1 can be confirmed, meaning that a larger number of board members contributes to the creation of value. The WPI (Women Participation Index) has a significance of 5% and a negative effect in the regression. However, the standardized coefficient is small, which refutes Hypothesis 2. The result suggests that higher participation of women on the board does not have a positive influence on firm value. The PDI (Professional Diversity Index) shows significance at the 10% level and a positive impact in the regression, though its standardized beta is low in magnitude. Thus, a positive sign was confirmed: greater professional diversity on the board results in a positive impact on firm value. Regarding the control variables, both are significant at the 1% level. Company size has a positive impact, with the highest standardized coefficient. Leverage (debt) shows a negative influence, being the second most significant element in the model.

Table 7

Firm Value through the Price to Book Multiple

Model |

Log Firm Value Price to Book 2019-2022 |

|

Beta (Unstandardized) |

Beta (Standardized) |

|

(Constant) |

0.936** (0.039) |

|

Number of Members |

0.096*** (0.001) |

0.221 |

WPI |

-0.393** (0.015) |

-0.078 |

PDI |

0.236* (0.077) |

0.063 |

Size |

0.904*** (0.001) |

0.798 |

Leverage |

-1.365*** (0.001) |

-0.292 |

*** 1%, ** 5%, * 10% sign.

Source: Prepared by the authors.

In statistical terms (Table 8), most of the explanatory variables are significant at least at the 10% level, except for PDI. In the case of the number of members, the coefficient is positive and statistically significant at the 1% level. Additionally, the standardized Beta is moderate; therefore, it confirms a positive relationship between board size and firm value.

Regarding the Women Participation Index (WPI), the sign is negative and it has a significance at the 5% level. The standardized coefficient is small, which leads to rejecting Hypothesis 2. A higher participation of women on the board does not seem to have a positive influence on the firm's value.

On the other hand, causality cannot be validated for PDI, as it has a significance level higher than 10%. The results do not allow us to accept or reject Hypothesis 3, but referring to the raw coefficient, it suggests a positive trend towards greater professional diversity on the board.

Finally, it is important to note that the variables' size and leverage have statistical significance at the 1% and 10% levels, respectively. The impact is positive in the case of size and negative for leverage. The standardized coefficient for the size variable is the one with the strongest impact on the regression. This is likely because the dependent variable is composed of revenue from sales, so it is expected that companies with a larger volume of assets will have more sales.

Table 8

Firm Value for the Price to Sales Multiple, 2019-2022

Model |

Log Firm Value Price to Sales 2019-2022 |

|

Beta (Unstandardized) |

Beta (Standardized) |

|

(Constant) |

-0,065 (0,914) |

|

Number of Members |

0,110*** (0,001) |

0,238 |

WPI |

-0,426** (0,049) |

-0,080 |

PDI |

0,267 (0,132) |

0,067 |

Size |

0,926*** (0,001) |

0,766 |

Leverage |

-0,401* (0,062) |

-0,075 |

*** 1%, ** 5%, * 10% sign.

Source: Prepared by the authors.

Table 9 expresses that, unlike the previous cases, there are fewer explanatory variables with high levels of significance, with the number of members, size, and indebtedness standing out, all of which have significance at the 1% level. In contrast, the WPI and PDI do not have a level of significance that allows for validating causality.

The number of members has a positive influence on the firm value, as indicated by the sign of the regression coefficient. Moreover, the unstandardized coefficient shows a moderate contribution to the regression, as it is the third most relevant coefficient. Therefore, it can be reaffirmed that there is a positive tendency for a larger board of directors to lead to higher firm value. On the other hand, the standardized coefficients of the WPI and PDI are of low magnitude in the regression; however, the regression signs reiterate the trends seen in the two previous models, with a negative sign for the WPI and a positive sign for the PDI. As with the previous cases, the board size received a positive sign, and it is also the standardized coefficient with the highest value. Indebtedness, on the other hand, showed a negative impact of lower magnitude.

Table 9

Firm Value for the Ev to Ebitda Multiple, 2019-2022

Model |

Log Firm Value Ev to Ebitda 2019-2022 |

||

Beta (Unstandardized) |

Beta (Standardized) |

||

(Constant) |

-0,303 (0,587) |

|

|

Number of Members |

0,070*** (0,001) |

0,154 |

|

WPI |

-0,117 (0,544) |

-0,022 |

|

PDI |

0,164 (0,320) |

0,040 |

|

Size |

1,001*** (0,001) |

0,830 |

|

Leverage |

-0,506*** (0,009) |

-0,098 |

|

*** 1% , ** 5%, * 10% sign.

Source: Prepared by the authors.

Discussion

The composition of BODs in Chile presents some notable characteristics, including an average size of around 7.9 members, as nearly 90% of companies have either 7 or 9 directors. The participation of women remains low, at 9% in 2019, though there is a trend towards greater inclusion, as by 2022, women represent 17% of board members. The Professional Diversity Index (PDI) is moderately high, with a mean fluctuating between 0.62 and 0.64 each year of the study, indicating a tendency towards professional heterogeneity.

These structural characteristics of Chilean BODs are similar to findings from other studies in Latin America. In terms of female participation, despite efforts in recent years, it remains low, though statistically significant increases have been noted when compared to previous studies such as those by Arenas et al. (2020), Arévalo et al. (2020), and Rosas et al. (2023), where the presence of women on boards was under 10%. Furthermore, the most common professional backgrounds among Chilean BODs align with the study by Cruzat et al. (2021) on publicly listed companies in Brazil, highlighting fields such as engineering, business administration, and law.

The results indicate that the number of BODs is the independent variable with the greatest impact, showing a high degree of significance across all three regression models, thereby confirming the first research hypothesis. A positive relationship exists between board size and economic value. This is supported by the idea that greater information exchange enhances board efficiency (Lehn et al., 2009). However, it is important to note that the majority of boards have either 7 or 9 members. In this regard, adding one more member could, at some point, have a negative effect, as seen in the studies by Pucheta (2015) and King et al. (2018).

Regarding the Women's Participation Index (WPI), there is a negative relationship with value creation in all three regression models applied. While the logarithmic values for Price to Book and Price to Sales show statistical significance, for the Logarithm of EV to EBITDA, the significance falls outside the acceptable ranges. Furthermore, the standardized coefficients indicate a low influence of the WPI variable in the regression. This suggests that results should be interpreted with caution. While a negative trend is observed, it may be due to a bias caused by the underrepresentation of women on boards. These results are consistent with research by Rosas et al. (2023), who argue that low female participation could lead to an overestimation of the positive effects of gender diversity, depending on the methodology used.

As for the PDI, there is a positive impact on firm value, but it is essential to highlight that it is the variable with the least statistical significance, with a 10% level in the Price to Book variable, and in the other two regressions, it does not show statistical significance to demonstrate causality. The standardized coefficients also exhibit a low influence on firm value. When focusing solely on the sign, the results align with prior studies that indicate a positive trend, such as Bantel (1993), who suggests that the benefits of professional diversity can be observed across various industrial sectors.

Conclusions

Regarding the number of board members, the coefficient is positive and statistically significant at the 1% level, and the standardized Beta is moderate. Therefore, this confirms Hypothesis 1, which suggests a positive relationship between the BoD size and company value. Concerning the Women's Participation Index (WPI), the coefficient is negative and statistically significant at the 5% level. Additionally, the standardized coefficient is small, which leads to rejecting Hypothesis 2: higher participation of women on the board does not appear to have a positive influence on the company’s value. On the other hand, causality in the Professional Diversity Index (PDI) cannot be validated, as it has a significance level above 10%. Thus, the results do not allow us to accept or reject Hypothesis 3, but when referring to the control variable of company size, it has the greatest impact across all three regression models.

As mentioned earlier, only the number of board members shows a moderate influence on company value. The results suggest that the variables of female participation and professional diversity on the board do not seem to have a significant impact on the company’s performance. If this is the case, then the company’s value is more likely to be conditioned by company size and other variables that are not explained by board composition.

This research is not without limitations. The primary limitation is the study period, as the companies in the sample may have been affected by the social crisis that occurred in Chile in the last quarter of 2019, the COVID-19 pandemic, which severely impacted global economies in 2020 and 2021, and the lingering economic repercussions of the pandemic in 2022, such as higher inflation and interest rates, among others.

Finally, for future research, one potential direction could be to create dummy variables to categorize female participation, including the number of women on each board. Additionally, a similar approach could be applied to professional diversity, creating two categories for board members: those with postgraduate degrees and those without.

Ethical Considerations

Conflict of Interest

All authors made significant contributions to the paper and declare that there is no conflict of interest related to this article.

Author Contribution Statement

Andrea King Domínguez: Conceptualization; Methodology; Research; Writing; Review and Editing.

Rosa Martha Ortega Martínez: Research; Writing; Review and Editing.

Luis Améstica Rivas: Conceptualization; Methodology; Writing: Review and Editing; Supervision.

Funding Source

References