Administration and Business

Capital simulation tools in educational and financial institutions

Herramientas simuladoras de capitales en entidades educativas y financiera

Ferramentas de simulador de capital em instituições educacionais e financeiras

By: 1Fabio Orlando Cruz Páez![]() ; 2Odair Triana Calderón

; 2Odair Triana Calderón![]()

1Master's in Organizational Administration, Universidad Nacional Abierta y a Distancia. Researcher at the Universidad de Cundinamarca. ORCID: 0000-0001-7834-2762. E-mail: focruz@ucundinamarca.edu.co. Facatativá - Colombia.

2Master's in Finance, Universidad Autónoma del Caribe. Professor at the Universidad de Cundinamarca. ORCID: 0000-0002-3288-474X. E-mail: odair@ucundinamarca.edu.co. Facatativá - Colombia.

Received: June 5, 2023 Accepted: October 23, 2024

DOI: https://doi.org/10.22267/rtend.252601.269

How to cite this article: Cruz, F. & Triana, O. (2025). Capital simulation tools in educational and financial institutions. Tendencias, 26(1), 165-190. https://doi.org/10.22267/rtend.252601.269

![]()

Abstract

Introduction: This research article explores the perception of the need to manage a simulation software or tool that allows for the improvement of skills in planning and decision-making from a financial management perspective. Objective: The main goal is to analyze the importance of financial simulation applications that professionals learn to use to improve personal and business finances. Methodology: The research was of a mixed type and approach, with a quasi-experimental design, a descriptive, cross-sectional, and field study scope, and the Delphi method was used. Results: The findings were established through the applied instrument, which was a structured interview with 25 financial experts based on two theoretical variables: the first is software application, and the second is management. Although some applications are used, experts tend to create their own tools to contribute to effective decision-making from basic to advanced levels. Conclusions: Based on this, it is concluded that decision-making by professionals, with or without postgraduate studies, is deeply influenced by their expertise and the effective handling and analysis of results obtained from free software, Excel add-ons, and paid applications, both at the personal and business levels.

Keywords: software application; credit; financing; management; investment.

JEL: D25; H81; L86; M11; P33.

Resumen

Introducción: El presente artículo de investigación aprecia la percepción sobre las necesidades de manejar una aplicación o herramienta informática de simulación, que permita mejorar las habilidades para la planeación y la toma de decisiones desde la gestión financiera. Objetivo: El objetivo principal es analizar la importancia de las aplicaciones de simulación financiera que los profesionales aprenden a gestionar con el fin de mejorar las finanzas personales y empresariales. Metodología: La investigación fue de tipo y enfoque mixto, con un diseño cuasi experimental, un alcance de estudio descriptivo, transeccional y de campo y se utilizó el método Delphi. Resultados: Los hallazgos se establecieron mediante el instrumento aplicado que fue una entrevista estructurada a 25 expertos en finanzas a través de dos variables teóricas, la primera es aplicación informática y la segunda es gestión. Aunque se manejan algunas aplicaciones, los expertos crean sus propias herramientas para contribuir a la asertiva toma de decisiones desde lo básico hacia lo avanzado. Conclusiones: Con base en ello, se concluye que la toma de decisiones de los profesionales con o sin posgrado, se ve inmersa en la experticia y asertivo manejo y análisis de los resultados obtenidos por software gratuitos, complementos de Excel y aplicaciones pagadas tanto a nivel personal como empresarial.

Palabras clave: aplicación informática; crédito; financiación; gestión; inversión.

JEL: D25; H81; L86; M11; P33.

Resumo

Introdução: Este artigo de pesquisa aprecia a percepção sobre a necessidade de manusear um aplicativo ou ferramenta de simulação computacional que permita aprimorar as habilidades de planejamento e tomada de decisão na gestão financeira. Objetivo: o objetivo principal é analisar a importância dos aplicativos de simulação financeira que os profissionais aprendem a gerenciar para melhorar as finanças pessoais e empresariais. Metodologia: a pesquisa foi de tipo e abordagem mista, com desenho quase experimental, escopo de estudo descritivo, transversal e de campo, e foi utilizado o método Delphi. Resultados: as conclusões foram estabelecidas por meio do instrumento aplicado, que foi uma entrevista estruturada com 25 especialistas em finanças por meio de duas variáveis teóricas: a primeira é o aplicativo de computador e a segunda é o gerenciamento. Embora alguns aplicativos sejam manipulados, os especialistas criam suas próprias ferramentas para contribuir com a tomada de decisão assertiva, desde o básico até o avançado. Conclusões: Com base nisso, conclui-se que a tomada de decisão de profissionais com ou sem pós-graduação, está imersa na expertise e no manuseio e análise assertiva dos resultados obtidos por softwares livres, suplementos do Excel e aplicativos pagos tanto em nível pessoal quanto empresarial.

Palavras-chave: aplicação informática; créditos; financiamento; gestão; investimento.

JEL: D25; H81; L86; M11; P33.

Introduction

In the current business and educational environment, software applications such as simulation tools are used in investment and financing. Given the significant need to predict the future, or at least have potential alternatives in the face of certain events, based on historical data, and internal and external variable behavior, financial simulation emerges as an alternative to mitigate uncertainty and make more informed decisions that aim toward future realities. This is considered both a training measure and a practice in financial management. Thus, the research aimed to answer the question: How does the use of financial software applications influence decision-making in management regarding investment and financing alternatives? Primary and secondary sources related to the theoretical variables—software application, financing, management, and investment—were explored to analyze the importance of financial simulation applications that professionals learn to manage for personal and business finance, focusing on effective decision-making.

Software Application

In the financial software field, among the most widely used tools are the Laboratorio de Simulación en Administración y Gerencia [Simulation Laboratory in Administration and Management] – LABSAG, and Risk Simulator, both for academics and professionals in the finance sector.

LABSAG

The specialized simulators of LABSAG include, first, SIMDEF, in the finance field, used in courses such as Financial Management, Managerial Accounting, Project Development and Evaluation, and Capital Markets; second, SIMPRO, in operations, used in courses like Production Management, Operations Management, Production Direction, and Quality Control; third, MARKESTRAT, in strategic marketing, used in courses like Market Strategy, Marketing Management, and Market Research, among others; fourth, MARKLOG, in marketing and logistics, B2B, used in courses such as Business-to-Business Marketing and Service Marketing and Business Logistics; and finally, ADSTRAT, in advertising management, used in courses like Marketing and Sales Management and Market Research (Díaz and Márquez, 2016, p. 67).

The LABSAG simulator package is available on the cloud; however, not all institutions have the financial capacity to access it, especially universities. This situation highlights the importance of searching for similar alternatives with simpler, more practical models that fulfill the purpose of addressing gaps and generating soft skills in students, thus contributing to improving financial literacy.

LABSAG (2009) (as cited in Mendoza, 2015) states that the use of these simulators provides benefits such as the application of knowledge to solve problems, better knowledge transfer and retention, a better understanding of abstract concepts, and increased motivation among students.

LABSAG is a business simulator that integrates the best simulators used and designed in Europe and the United States into a single platform. It is used by universities as a means of training professionals, as it contains various components, including TEMPOMATIC, a comprehensive tool that offers students a range of alternatives in a case study. This case has eight periods with their respective reports and provisions, and the task is to make decisions in production, marketing, finance, and other areas to consolidate the company, where each created industry competes with others to obtain higher profits.

TEMPOMATIC facilitates the perspectivist management approach, the analysis of financial information, and the blending of productive factors in order to improve products and services in the long term (Recalde, 2013, p. 38).

LABSAG provides the power to manage, install, train, and advise organizations on the use and management of business simulators in order to enhance managerial competencies of human capital. It provides an integrated platform that trains individuals in universities in any disciplinary field related to finance, serving both students and organizational employees (Garzón, 2012, p. 54). The company organizes events where participants can compete using the simulator, called the “LABSAG Challenge”. Being a cloud-based simulator, its use may be costly for an individual or small business, and it is mainly used by universities.

In Colombia, there are currently 15 universities using LABSAG out of over 120 universities in Latin America. Some of the universities that hold a license for academic use in training professionals in business administration, finance, accounting, industrial engineering, and other fields include the Universidad Militar Nueva Granada, Universidad Santo Tomás, Universidad Cooperativa de Colombia, Universidad del Tolima, Universidad Autónoma del Caribe, Fundación Universitaria del Área Andina, Universidad Nacional Abierta y a Distancia – UNAD, among others. Similarly, countries such as Mexico, Honduras, El Salvador, Ecuador, Costa Rica, Bolivia, Argentina, Peru, Chile, and Spain also use the simulator (LABSAG, 2021).

Risk Simulator

Risk Simulator is a tool used in finance, statistics, econometrics, and risk assessment.

In variable-income investments, such as investment projects, once cash flows and indicators like Net Present Value (NPV) and Internal Rate of Return (IRR) are calculated, they contribute to creating risk scenarios through sensitivity analysis of the indices, aiming to provide better decision-making support. According to Inquilla and Rodríguez (2019, p. 165), Risk Simulator is used to manage the minimization of economic losses inherent to risks occurring in Colombian entities, implementing a Monte Carlo simulation.

Thus, when simulating the model with Risk Simulator in relation to output variables like NPV and IRR, the level of forecast accuracy is observed in order to determine the number of attempts to simulate through precision and error control, which is facilitated by the program (Inquilla and Rodríguez, 2019, p. 170).

Like LABSAG, Risk Simulator is widely used by universities and technical institutions such as the Servicio Nacional de Aprendizaje (SENA), Politécnico Gran Colombiano, Universidad del Valle, Universidad Externado de Colombia, Universidad Nacional de Colombia, Universidad Central, and Universidad Autónoma de Bucaramanga. Additionally, this tool is also employed in the real sector by entities like Porvenir, Seguros Bolívar, and various banking institutions in countries such as Venezuela.

It is important to note that Risk Simulator is used as a complement to Microsoft Excel, functioning as an additional component, with its operation based on models constructed in this spreadsheet. Due to its high cost for individuals seeking to make investments, its use is limited to business idea formulation by advisors, who use it to establish a more objective parameter for the alternatives and risks involved in investing in a productive project. As an educational tool, it includes a trial simulator and support videos for different evaluation cases on YouTube.

@Risk

Like Risk Simulator, @Risk is a very comprehensive simulator; perhaps it is more user-friendly. However, it is necessary to have a solid knowledge of management, finance, and economics to interpret the data obtained. The @Risk model is very similar to that of Risk Simulator; as a complement to Microsoft Excel, it offers alternatives for obtaining forecasts and analyzing financial variables in order to generate different risk scenarios. Additionally, it provides a time-limited demo and training through its virtual platform or the PALISADE website. They consistently send information about real-time activities, such as webinars, via email.

Sánchez and Uribe (2017) assert that @Risk is useful in productive projects to assess optimistic, favorable, and pessimistic scenarios regarding input variables in the cash flow model, starting from a distribution that can be adjusted to the available data in the project.

Investment and Financing Simulators (Colombian Financial System - CFS)

For personal finance, it is essential to have financial education and tools that allow individuals to evaluate decisions related to investment and financing. To this end, companies belonging to the CFS, particularly credit institutions, have engaged with users through their websites, providing clearer and more straightforward information.

It is important to highlight that, according to Banco de Bogotá (2024a), as affirmed through the study conducted by the specialized magazine Global Finance, it is currently the best bank in Colombia. This recognition is due to the fact that the institution offers services with greater acceptance than other banks, providing reliability through its technological innovation in products and/or services such as loans, savings accounts, mortgages, insurance, and credit and debit cards, among others.

However, in most cases, the financial simulation interface of banks is not very user-friendly, does not generate clear and understandable information, or is insufficient. Despite this, these tools are of vital help to users, as long as they clearly understand interest rates, amortization models, and interest calculations, which helps them make the most of the products the banks offer.

In Colombia, institutions such as Davivienda (2024), Bancolombia (2024), Banco de Occidente (2024), and Banco de Bogotá (2024b) offer financial simulators, as do AV Villas, BBVA (2024), and Banco de Santander (2024). A positive aspect is that these simulators are free and provide essential assistance when considering credit alternatives, TDCs, or other options like leasing.

Microsoft Excel

Finally, the spreadsheet, commonly known as Excel, offers a series of add-ins that, when combined with the basic elements of the Microsoft application, can be a very important simulation tool. Additionally, they are the operational medium for simulators such as Risk Simulator and @Risk. According to Castro (2017), in investment projects, consultants are hired to evaluate quantitative data using Excel, generating indicators for effective decision-making.

Among the most commonly used add-ins in Excel for financial modeling are: VLOOKUP, AVERAGE, GOAL SEEK, DATA TABLE, SCENARIO MANAGER, SOLVER, NOMINAL, PMT, EFFECTIVE, FV, PV, NPV, among many others. When combined with a modeling tool, these can generate a very useful and interesting instrument. As a curious fact, in Excel 2010, a single sheet in a workbook contains 1,048,756 rows and 16,384 columns, resulting in a total of 17,182,818,304 cells on just one sheet, which indicates that the amount of information that can be incorporated is very high.

Credits

Credit institutions facilitate investments and loans for individuals and businesses in Colombia, and provide support to SMEs that generate employment through operations that enhance business liquidity (Rodríguez, 2019, p. 9). One of the most important actions in granting and/or assessing the viability of loans and/or investments is the credit score of individuals and legal entities, as, according to García (2020, p. 22-23), the evaluation is generated based on the legal guidelines of the institution and applied by financial experts to assist interested parties.

In banking institutions, guidelines are established to provide services to individuals and businesses in order to assist both civil society and organizations. According to Leal et al. (2018, p. 183), banks tend to overlook smaller financial institutions, as an adequate investment and/or loan management process requires directing and correcting credit management through assertive, detailed, and effective decision-making. Regarding financial tools, credits can help improve individuals' quality of life when there is proper planning through saving and investing, fully meeting the commitments acquired from financing (Betancur et al., 2019, p. 37).

Financing

Financing is a fundamental part of the global context for the development of activities, sales, and the acquisition of services and products. Therefore, in the education of individuals from childhood, the teaching-learning process is vital to optimize the acquisition of financial resources and the assertive use of financial tools, as mentioned earlier, for example, in the case of leveraging credit. According to Lancheros and Mora (2022), in order to achieve socioeconomic development in countries like Colombia, science, technology, and innovation in higher education help promote financial security and the management of resources obtained from a financing system. Once allocated, these resources should be used in the professional training of individuals to facilitate assertive decision-making and management.

According to Chagerben et al. (2017), there is invariably a pressing relationship between sales and assets. For this reason, the economic growth index governs the increase in assets, which is reflected in the financing needs of organizations.

Regarding intangible assets, it is observed that these provide growth opportunities in the future, thanks to the competitive advantages they can generate (Neville & Lucey, 2022).

According to Barona et al. (2017), in Colombia, business assets were part of the proposal to improve investment in innovation, technology, and entrepreneurship, generated through financing from public and/or private sources based on grants or tax exemptions, or initial and risk capital.

The aforementioned aims to acknowledge successful contributions to the real economic sector, highlighting the assertive management of resources for personal and business financing in Colombian society, as well as the ability to make sound investments. According to Chen et al. (2022), loans granted to SMEs occur when financing is managed with friends and family.

According to Gopalakrishnan et al. (2022), regarding company financing requests, it is currently observed that companies with physical offices are more numerous than those that allow remote work in their teams. Similarly, in personal and business financing, Xia et al. (2022) affirm that digital finance, through the appropriation of remote interactions, facilitates business development in and post-pandemic (COVID-19).

Investment

Investment is the action undertaken by an individual and/or legal entity to obtain benefits from the production, service provision, and/or satisfaction of personal and third-party needs. In investment projects, this is understood, according to Andia (2010), as an intervention in different mediums to solve existing problems or generate desired changes in the face of limitations or excesses of goods and/or services.

According to Barona et al. (2017), investing in machinery and equipment is made accessible through bank financing, while using own resources is the best option for financing intangible assets that are not financed by banks. Ramesh and Rao (1989) (as cited in Chagerben et al., 2017) state that the investment decision is the response to the questions: How much should be invested to enhance productivity? And in which specific assets should the investment be made?

In the investment activities of individuals and legal entities (businesses), competitiveness is promoted; therefore, according to Farooq et al. (2022), it is important to recognize the behavior of business investments through the rate of return, short payback periods, and the availability of financing sources.

One key factor affecting investments in countries is the value of the currency, as foreign investors with significant purchasing power can invest in local businesses. Thus, Edo and Kanwanye (2022) argue that foreign portfolio investors thrive in economies where the local currency value is low, and this is why the value of the currency has a direct impact on investments.

When it comes to investments, it is important to highlight, among other factors, the behavioral finance of investors, as these influence the capacity to invest based on decision-making. As such, ul Abdin et al. (2022) state that financial behaviors explore divergent factors that have a significant influence on investment decisions and the performance of investors, primarily in terms of the satisfaction it brings them. Similarly, according to Cruz et al. (2022, p. 38), investment shows that undergraduate education provides access to important information that promotes assertive decision-making.

It is also crucial to emphasize that investment is based on the ability to make decisions and the rigorous study of events that occur in a globalized context. According to Hoang et al. (2022), it is evident that companies with higher degrees of irreversibility in their investments typically make fewer investments than their competitors, due to the efforts made by governments to mitigate the negative impacts caused by the pandemic.

In essence, investment decisions made in the professional realm contribute to seizing various opportunities for financial capital growth. Therefore, the risky decisions made by expert investors on behalf of others strengthen the finances of individuals and/or legal entities. For example, some studies confirm that experts tend to take on more risk for their clients than they would for themselves (Kling et al., 2022).

Management

Financial management is the decision-making process regarding the different alternatives available to address financial situations or needs. This adds value to management, as its main function is to continuously make decisive and assertive decisions (García, 2022).

Financial management or decision-making occurs assertively in direct relation to planning and control. Essentially, individuals and companies must continuously project future investments and the ways in which they will be financed, in order to manage the continuous verification of decisions that impact financial outcomes (Chagerben et al., 2017, pp. 792-793).

Thus, in management, according to Cruz et al. (2020), the financial intelligence of university students and individuals, in general, is part of the change in each person's behavior in the market, contributing to assertive financial management.

In business administration, human capital, which is part of a society's workforce embedded in companies, facilitates decision-making for assertive organizational management, promoting growth among the involved parties: employees, customers, suppliers, and business owners.

In this way, Rojas and Espejo (2020) state that human capital refers directly to both tacit and explicit knowledge in the pillars of knowledge: know-how, know-what, and being, which demonstrate the competencies derived from the experience and talent of human capital. Therefore, the competencies individuals possess in managing actions within businesses and in their personal lives are an essential part of financial management in real and desired contexts.

Methodology

The methodology used was of a mixed type and approach, as it incorporates evidence from numerical, verbal, textual, visual, symbolic, and other types of data (Hernández et al., 2014), in order to understand problems and events in real contexts regarding the use of financial tools for decision-making.

The design is quasi-experimental, as it involved analyzing the responses of experts in financial simulation concerning the applications conducted in the study (Cruz et al., 2020).

The scope of the research is a descriptive, cross-sectional, and field study, as it investigates the occurrence or level of one or more variables in the populations studied (Cruz et al., 2019) and was conducted at a single point in time.

The interview applied was of the Delphi type, consisting of 15 Likert-scale questions and one open-ended question, totaling 16 questions. It was carried out during September 2021, in which it can be inferred that:

The Delphi method considers converging expressions of opinion and involves inherent consensuses on specific topics, carried out through questions directed at experts. The most frequent objective of studies using the Delphi type is to contribute from the experts' experience on areas of indecision, with the purpose of strengthening decision-making (Mera et al., 2015).

Results

The research instrument was applied to 25 experts in the financial field, including business administrators, public administrators, financial administrators, economists, international relations specialists, civil engineers with degrees in commerce, and accountants. Of these, 36% finished an undergraduate program, 32% are specialists, 24% are master's degree holders, and 8% hold doctoral degrees. These experts work in Colombia's financial system, in the financial sector, as educators, and in the commercial field.

The experts' perceptions regarding the variables considered when evaluating their decisions in management and the use of simulation tools were as follows:

Financial Simulation Software

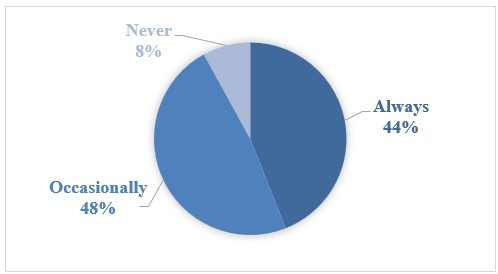

Figure 1 shows the use of financial simulation tools.

Figure 1

Use of Financial Simulation Tools

Source: Prepared by the authors.

The first question refers to the use of financial simulation tools in their professional training, which showed that 44% always used these types of tools, while 8% never did; however, 48% used them to a moderate extent.

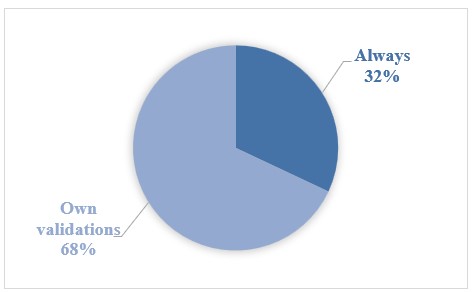

Next, Figure 2 presents the experts' confidence in the truthfulness and effectiveness of financial tools.

Figure 2

Confidence in the truthfulness and effectiveness of financial tools

Source: Prepared by the authors.

An important aspect is whether, when using financial simulation tools, there was confidence in the truthfulness and effectiveness of the results for decision-making. 32% always trusted the results, while 68% showed some degree of mistrust, possibly due to their knowledge, with some conducting their own validations.

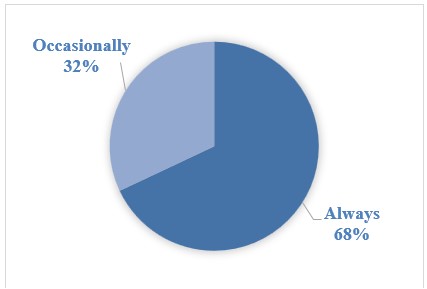

Figure 3 is presented, showing the use of financial tools as a didactic learning strategy.

Figure 3

Use of Financial Tools as a Didactic Learning Strategy

Source: Prepared by the authors.

Regarding the consideration of using simulation tools as a didactic strategy to facilitate learning in finance, the perception is very positive. 68% of the focus group indicated that these tools should always be used in academia, while 32% stated that they should be used to some extent.

In consideration of the importance of having more financial simulation tools in the market to strengthen financial training processes, the message is clear: 70% believe they should always be used.

Regarding the use of free-access financial simulation tools available online, the result was that 28% stated they have never used them, due to their limited availability; 44% use them partially, and 28% have always used them.

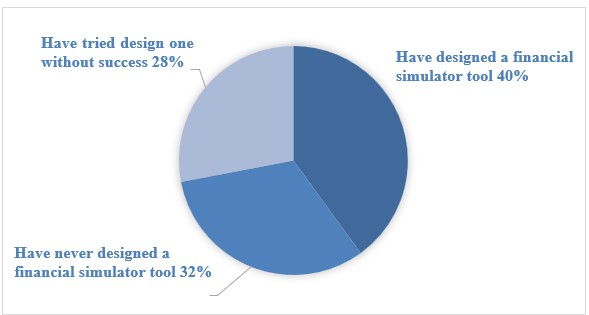

Figure 4 addresses the creation of custom tools by financial experts.

Figure 4

Design of Custom Tools by Financial Experts

Source: Prepared by the authors.

An important point highlighted by the experts was that 40% of them have designed a financial simulation tool themselves using Excel or other office software programs. Only 28% have not done so, which confirms that the limited availability or cost of these simulators leads them to create their own resources. Meanwhile, 32% have tried to design one without success.

On the other hand, some experts mentioned that they have always faced technical and technological difficulties when using financial simulators for decision-making, with 59% affirming this, while the rest experienced these difficulties occasionally.

Regarding proposing alternatives to improve the functionality of the simulators they have used, 44% stated that they never do so, 50% do so occasionally, and 6% always try to make improvements. This is important for developing new and better versions of these tools.

Management

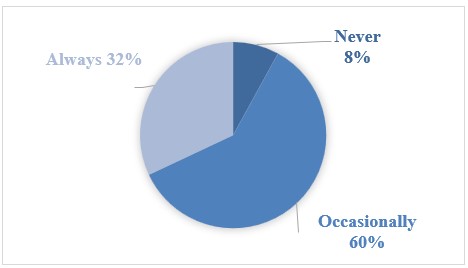

Figure 5 is related to the decision-making process regarding professional or academic projections using financial applications.

Figure 5

Decision-making for Professional or Academic Projects Using Financial Applications

Source: Prepared by the authors.

Next, the question asked whether, when developing a professional or academic project that requires investment decision-making, they had used financial applications to assess its viability. The results showed that 8% of respondents had never done so, 60% do it occasionally, and 32% always use them. This indicates that the use of tools to evaluate an alternative is crucial in the analysis process.

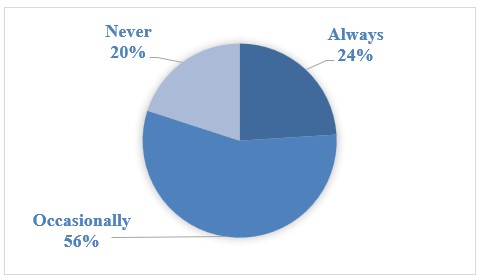

Figure 6 shows the usability of financial applications for decision-making in family projects.

Figure 6

Use of Financial Applications for Decision-making in a Family Project

Source: Prepared by the authors.

In the question related to the entrepreneurship of a family project, such as the acquisition of an asset, respondents were asked about the use of financial applications that enable effective decision-making. The results showed that 24% always use these applications, 56% use them occasionally, and only 20% have never used them.

These experts believe that the use of financial simulation tools is easy to manage and apply to solving everyday problems, which suggests that their use helps improve financial decision-making. Of the respondents, 48% stated that financial tools should always be used this way, while 52% mentioned that they make decisions daily that affect their family's finances.

Finally, they were asked: If allowed to apply a new simulator for financial decision-making, what aspects would you consider important in the design of this tool? Some of the statements are presented in Table 1.

Table 1

Aspects to Consider in the Application of a New Financial Decision-Making Simulator

Surveyed Person |

Response |

J. Roa (personal communication, September 30, 2021) |

"I would focus on making it easy to use and understand for anyone, so they don't have to take an extensive course to learn how to use and read it, but rather make life easier for students or people who want to use it in their everyday lives." |

Y. Sánchez (personal communication, September 30, 2021) |

"Offline functions." |

J. Mayorga (personal communication, September 30, 2021) |

"The quality of the information, knowledge about the topic." |

N. González (personal communication, September 30, 2021) |

"Interest rates." |

J. Zamora (personal communication, September 30, 2021) |

"It should be grounded in reality." |

M. Rodríguez (personal communication, September 30, 2021) |

"I believe it would be important for the tool to generate an amortization table that distinguishes between the amount for capital, interest, and other concepts in the simulation for a more accurate decision-making process." |

A. Manrique (personal communication, September 30, 2021) |

"The data provided by the tool should be continuously updated, and when it comes to investment, it must be connected in real-time to the data from various global stock exchanges and have access to the financial statements of leading international market companies." |

J. Rivera (personal communication, September 1, 2021) |

"The data provided by the tool should be continuously updated, and when it comes to investment, it must be connected in real-time to the data from various global stock exchanges and have access to the financial statements of leading international market companies." |

J. González (personal communication, September 30, 2021) |

"It should be educational and easy to learn, so users can apply it correctly and be confident in their usage." |

C. Arévalo (personal communication, September 30, 2021) |

"Profitability over time." |

P. Rodríguez (personal communication, September 30, 2021) |

"Basic knowledge." |

O. Vanegas (personal communication, September 30, 2021) |

"It should be developed in an easy-to-understand way, with comprehensible language, not technical language." |

O. Castillo (personal communication, September 30, 2021) |

"Profitability over time." |

L. Rangel (personal communication, September 30, 2021) |

"Basic knowledge." |

Y. Rodríguez (personal communication, September 30, 2021) |

"Ease of handling and analysis of results." |

J. Correa (personal communication, September 30, 2021) |

"It should be developed in an easy-to-understand way, with comprehensible language, not technical language." |

Source: Prepared by the authors based on personal interviews.

This table shows the aspects that the experts considered important for the application of a new simulator, where the statements highlight the importance of the simulator’s ease of use with comprehensible language. It also emphasizes the basic financial knowledge that individuals using it should have, as well as the accessibility to the design of future scenarios that reflect the possible reality of investment for proper decision-making.

Thus, the financial tools, according to the research conducted and the contributions from the experts, offer valuable insight that the decision-making process of young people and their family members can continuously improve with the assertive use of simulation tools. This, in combination with their understanding and analysis, helps in managing different resources in personal, family, and business projects.

Conclusions

Once the study on the use of simulation tools for various investment and financing alternatives in personal finance, both at the educational and financial levels (such as simple interest and compound interest), was conducted, it was concluded that the research was important. It allowed for the identification, across various fields of management and finance, and among professionals in the areas studied, of the protocol they follow when making investment or financing decisions. The use of a simulator or tool is of great importance to 50% of the participants, as it allows them to understand the behavior, cost, or return of an operation, thus helping to steer the process in a favorable direction.

Additionally, thanks to the use of financial simulation tools, new research is being contributed to regarding interest rates applied to financial decisions, the most commonly acquired or requested credit lines by families, the reasons behind low interest in personal savings for different purposes, and financial education and culture among young people, among others.

Regarding TDCs and leasing, these are alternatives not only for companies but also for individuals within the Colombian financial system. Financial simulation tools facilitate decision-making for the assertive use of these resources that are available to people in Colombia.

In light of the empirical findings related to modeling tools in investment and financing operations, and addressing the objective of the research, it was confirmed that it is essential to have basic tools that allow the owner of economic resources to manage them adequately. These tools must provide information so that the user can establish the best investment option or the most economical alternative that incurs fewer financial costs, should the case involve financing. This aspect is related to the appropriation of concepts and terms linked to finance. On the other hand, methods are deployed to determine possible alternatives for returns on investment, as well as the costs of producing a good or service and the financial risks that may arise from investing in fixed income or variable income.

Ethical Considerations

This study did not require approval from an Ethics or Bioethics Committee as it did not involve any living resources, agents, biological samples, or personal data that pose any risk to life, the environment, or human rights.

Conflict of Interest

All authors made significant contributions to the document and declare that there is no conflict of interest related to this article.

Author Contributions

Fabio Orlando Cruz Páez: Theoretical Framework, Methodology, Writing, Analysis, Review, and Editing.

Odair Triana Calderón: Research, Data Collection and Analysis, Writing, Project Management.

Funding Source

This article is the result of the research project "Herramienta de modelación financiera en operaciones de inversión y financiación en escenarios de renta fija o variable [Financial Modeling Tool in Investment and Financing Operations in Fixed or Variable Income Scenarios]" at the Universidad Autónoma del Caribe.

References

(1)Andia, W. (2010). Proyectos de inversión: Un enfoque diferente de análisis. Industrial Data, 13(1), 28-31. https://doi.org/10.15381/idata.v13i1.6154

(2)Banco de Bogotá. (2024a). Banco de Bogotá, Mejor Banco en Colombia 2024. https://saladeprensa.bancodebogota.com/2024/05/08/banco-de-bogota-mejor-banco-en-colombia-2024/

(3)Banco de Bogotá. (2024b). Simulador de crédito libre inversión. https://www.bancodebogota.com/wps/themes/html/digital/credito-libre-destino/simulador-credito.html

(4)Banco de Occidente. (2024). Simulador de crédito. https://www.bancodeoccidente.com.co/solicitarcredito/#/

(5)Banco de Santander. (2024). CDT Santander. https://www.cdt.santander.com.co/cdt-simulador

(6)Bancolombia. (2024). Simuladores y comparadores. https://www.bancolombia.com/centro-de-ayuda/simuladores-comparadores

(7)Barona, B., Rivera, J. A. y Garizado, P. A. (2017). Inversión y financiación en empresas innovadoras del sector servicios en Colombia. Revista Finanzas Y Política Económica, 9(2), 345–372. https://doi.org/10.14718/revfinanzpolitecon.2017.9.2.7

(8)BBVA. (2024). Simulador de Crédito. https://www.bbva.com.co/personas/servicios-digitales/simuladores.html

(9)Betancur, Y. M., Loaiza, V., Usuga, Y. y Correa, D. A. (2019). Determinantes del uso de herramientas financieras: análisis desde las finanzas personales. Science of Human Action, 4(1), 33-58. https://doi.org/10.21501/2500-669X.3118

(10)Castro, Z. I. (2017). Evaluación de proyectos de inversión para pequeñas y medianas empresas con una estrategia de proyección financiera. Ra Ximhai, 13(3), 15-40. https://doi.org/10.35197/rx.13.03.2017.01.zc

(11)Chagerben, L. E., Yagual, A. M. y Hidalgo, J. X. (2017). La importancia del financiamiento en el sector microempresario. Dominio De Las Ciencias, 3(2), 783–798. https://doi.org/10.23857/dc.v3i2.354

(12) Chen, B., Zhang, C. & Saydaliev, H. B. (2022). Does bank complexity during the COVID-19 crisis alter the financing mechanism for small and medium-sized enterprises? Economic Analysis and Policy, 75, 705-715. https://doi.org/10.1016/j.eap.2022.06.018

(13)Cruz, F., Castillo, D., Lechuga, J. y Triana, O. (2022). Conducta financiera en estudiantes de Administración de Empresas, Universidad de Cundinamarca Facatativá. Tendencias, 23(2), 30-52. https://doi.org/10.22267/rtend.222302.200

(14)Cruz, F., Ibarra, C., Rueda, D. y Olivares, D. (2020). Análisis exploratorio sobre la apreciación de características predominantes en empresas medianas de México y Colombia en temas de calidad, competitividad, innovación social y productiva. Tendencias, 21(1),130-156. https://doi.org/10.22267/rtend.202101.130

(15)Cruz, F., Mera, C. y Lechuga, J. (2019). Evaluación de estrategias de emprendimiento sostenible e innovación implementadas en las unidades productivas del SENA, Centro Industrial y Desarrollo Empresarial de Soacha-Cundinamarca-Colombia. Tendencias, 20(1), 183-202. https://doi.org/10.22267/rtend.192001.113

(16)Cruz, F.O., Castillo, D.M. y Lechuga, J.I. (2020). Innovación e inteligencia financiera en estudiantes de básica media del Instituto Diversificado Albert Einstein, Mosquera Cundinamarca. En W. R. Pinillos. (Ed.), Procesos de investigación con mirada translocal (pp. 51 – 72). Editorial de la Universidad de Cundinamarca https://repositorio.ucundinamarca.edu.co/bitstream/handle/20.500.12558/3213/Procesos%20de%20Investigacio%cc%81n%20sept%2030%20%281%29.pdf?sequence=1&isAllowed=y

(17)Davivienda. (2024). Simuladores. https://www.davivienda.com/wps/portal/personas/nuevo/personas/informacion_adicional/simuladores