https://doi.org/10.22267/rtend.26272.305

Review article

Corporate finance

Capital structure in Colombian SMEs: a semi-systematic literature review from trade-off, pecking order, agency, and psychological empowerment perspectives

Estructura de capital en las pymes colombianas: una revisión semisistemática de la literatura desde las perspectivas del trade-off, el pecking order, la agencia y el empoderamiento psicológico

Estrutura de capital nas PMEs colombianas: uma revisão semi-sistemática da literatura sob as perspectivas de trade-off, pecking order, agência e empoderamento psicológico

By: Zuray Andrea Melgarejo Molina![]() 1; Mayda Alejandra Calderon-Diaz

1; Mayda Alejandra Calderon-Diaz![]() 1;Felipe Alejandro Torres-Castro

1;Felipe Alejandro Torres-Castro![]() 1

1

1 PhD in Flexible Management Systems, Public University of Navarre, Pamplona, Spain. Associate Professor, Faculty of Economics, National University of Colombia, ORCID: 0000-0001-6651-6964. E-mail: zamelgarejomo@unal.edu.co, Bogotá - Colombia.

2 PhD in Economics, National University of Colombia. Postdoctoral Researcher, Faculty of Economics, National University of Colombia. ORCID: 0000-0001-6591-7184. E-mail: maacalderondi@unal.edu.co, Bogotá - Colombia.

2 Master's in Management, National University of Colombia. PhD Student, Los Andes University. ORCID: 0009-0002-4046-4419. E-mail: f.torrescastro@uniandes.edu.co, Bogotá - Colombia.

Received: December 15, 2025 Accepted: June 10, 2026

DOI: https://doi.org/10.22267/rtend.26272.305

How to cite this article: Melgarejo, Z., Calderon, M. & Torres, F. (2026). Capital structure in Colombian SMEs: a semi-systematic literature review from trade-off, pecking order, agency, and psychological empowerment perspectives. Tendencias, 27(2), 292-315. https://doi.org/10.22267/rtend.26272.305

![]()

Abstract

Introduction: Capital structure remains a central topic in corporate finance, particularly in emerging economies where institutional constraints, governance mechanisms, and managerial behavior influence financing decisions. Understanding capital structure in Colombian SMEs requires integrating multiple theoretical perspectives. Objective: To analyze the theoretical and empirical evidence on capital structure decisions in Colombian SMEs from the perspectives of Trade-Off Theory, Pecking Order Theory, Agency Theory, and Psychological Empowerment. Methodology: A semi-systematic literature review was conducted following the PRISMA 2020 guidelines. Searches were performed in Scopus and Web of Science between March and May 2025. The selection process included identification, screening, eligibility assessment, and inclusion, resulting in 27 studies for analysis. Results: No single theory fully explains financing decisions in Colombian SMEs. Trade-Off and Pecking Order theories explain leverage and financing preferences, Agency Theory highlights ownership structures and information asymmetries, and Psychological Empowerment emphasizes managerial autonomy and behavioral influences. Discussion: Capital structure decisions arise from the interaction of financial, governance, and behavioral factors shaped by firm characteristics and institutional conditions. Conclusions: A multidimensional perspective provides a more comprehensive understanding of capital structure decisions in Colombian SMEs. The study contributes by integrating financial, organizational, and behavioral explanations and identifying avenues for future research.

Keywords: behavioral finance; corporate governance; financing decisions; information asymmetry; managerial behavior.

JEL: D23; G32; G41; L25; M10.

Resumen

Introducción: La estructura de capital sigue siendo un tema central en las finanzas corporativas, particularmente en las economías emergentes, donde las restricciones institucionales, los mecanismos de gobernanza y el comportamiento gerencial influyen en las decisiones de financiamiento. Comprender la estructura de capital en las pymes colombianas requiere integrar múltiples perspectivas teóricas. Objetivo: Analizar la evidencia teórica y empírica sobre las decisiones de estructura de capital en las pymes colombianas desde las perspectivas de la teoría del Trade-Off, la teoría del Pecking Order, la teoría de la Agencia y el Empoderamiento Psicológico. Metodología: Se realizó una revisión semisistemática de la literatura siguiendo los lineamientos PRISMA 2020. Las búsquedas se efectuaron en Scopus y Web of Science entre marzo y mayo de 2025. El proceso de selección incluyó identificación, cribado, evaluación de elegibilidad e inclusión, dando como resultado 27 estudios para el análisis. Resultados: Ninguna teoría por sí sola explica plenamente las decisiones de financiamiento en las pymes colombianas. Las teorías del Trade-Off y del Pecking Order explican el apalancamiento y las preferencias de financiamiento, la teoría de la Agencia destaca las estructuras de propiedad y las asimetrías de información, y el Empoderamiento Psicológico enfatiza la autonomía gerencial y las influencias conductuales. Discusión: Las decisiones de estructura de capital surgen de la interacción entre factores financieros, de gobernanza y conductuales, configurados por las características de la empresa y las condiciones institucionales. Conclusiones: Una perspectiva multidimensional ofrece una comprensión más completa de las decisiones de estructura de capital en las pymes colombianas. El estudio contribuye al integrar explicaciones financieras, organizacionales y conductuales, e identificar rutas para investigaciones futuras.

Palabras clave: finanzas conductuales; gobierno corporativo; decisiones de financiamiento; asimetría de información; comportamiento gerencial.

JEL: D23; G32; G41; L25; M10

Resumo

Introdução: A estrutura de capital continua a ser um tema central nas finanças empresariais, particularmente nas economias emergentes, onde as restrições institucionais, os mecanismos de governação e o comportamento da gestão influenciam as decisões de financiamento. Compreender a estrutura de capital nas PME colombianas requer a integração de múltiplas perspetivas teóricas. Objetivo: Analisar a evidência teórica e empírica sobre as decisões relativas à estrutura de capital nas PME colombianas a partir das perspetivas da teoria do Trade-Off, da teoria da Pecking Order, da teoria da Agência e do Empoderamento Psicológico. Metodologia: Foi realizada uma revisão semissistemática da literatura, seguindo as diretrizes PRISMA 2020. As pesquisas foram efetuadas no Scopus e no Web of Science entre março e maio de 2025. O processo de seleção incluiu a identificação, a triagem, a avaliação da elegibilidade e a inclusão, resultando em 27 estudos para análise. Resultados: Nenhuma teoria, por si só, explica plenamente as decisões de financiamento nas PME colombianas. As teorias do Trade-Off e da «Pecking Order» explicam o alavancamento e as preferências de financiamento; a teoria da Agência destaca as estruturas de propriedade e as assimetrias de informação; e o Empoderamento Psicológico enfatiza a autonomia de gestão e as influências comportamentais futuras. Discussão: As decisões relativas à estrutura de capital resultam da interação entre fatores financeiros, de governação e comportamentais, determinados pelas características da empresa e pelas condições institucionais. Conclusões: Uma perspetiva multidimensional proporciona uma compreensão mais completa das decisões relativas à estrutura de capital nas PME colombianas. O estudo contribui para integrar explicações financeiras, organizacionais e comportamentais, bem como para identificar vias para futuras investigações.

Palavras-chave: finanças comportamentais; governo corporativo; decisões de financiamento; assimetria de informação; comportamento dos gestores.

JEL: D23; G32; G41; L25; M10.

Introduction

The debate about how firms define their capital structure remains one of the most persistent questions in corporate finance since the seminal work of Modigliani and Miller (1958). Their Irrelevance Proposition argued that, under perfect markets and without taxes, a firm’s value is independent of its capital structure. A few years later, they revised their model (Modigliani & Miller, 1963), recognizing that the use of debt can generate tax benefits and thus create incentives for firms to seek an optimal balance between equity and liabilities. These ideas laid the groundwork for subsequent theories, particularly the Trade-Off and Pecking Order theories, which continue to shape contemporary research on financing decisions.

The Trade-Off Theory (TO) proposes that firms seek an optimal balance between the benefits and costs of debt financing (Shyam & Myers, 1994). In contrast, the Pecking Order Theory (PO) suggests that firms follow a hierarchy of financing preferences, relying first on internal funds, then on debt, and finally on equity issuance (Myers & Majluf, 1984). Although these theories provide influential frameworks for understanding financing decisions, their explanatory power may be limited in contexts characterized by financial constraints, information asymmetries, and institutional barriers, such as those faced by many small and medium-sized enterprises (SMEs).

In Latin America, and particularly in Colombia, financial management represents a decisive factor for business growth and survival. Small and medium-sized enterprises (SMEs) account for over 99% of firms and approximately 75% of formal employment (Organisation for Economic Co-operation and Development [OECD] & Economic Commission for Latin America and the Caribbean [ECLAC], 2012). Despite their economic relevance, Colombian SMEs often face significant barriers to accessing external financing. Studies such as Vera and Mora (2013) report that many firms maintain lower-than-optimal debt levels, reflecting not only financing preferences but also restrictions in access to formal credit and institutional conditions that influence financing opportunities. These challenges raise questions about the extent to which traditional capital structure theories adequately explain financing decisions in emerging economies.

The COVID-19 pandemic further exposed these structural weaknesses. Despite government initiatives aimed at improving liquidity conditions, many SMEs continued to depend on informal financing mechanisms and personal guarantees. Torres et al. (2025) show that increases in the cost of capital significantly reduce returns on assets in Colombian SMEs, highlighting their vulnerability to financing constraints and adverse economic conditions.

These dynamics suggest the need to complement traditional financial explanations with broader theoretical perspectives. Agency Theory (Jensen & Meckling, 1976) contributes to understanding how conflicts of interest, information asymmetries, and governance mechanisms influence financing decisions. Likewise, Psychological Empowerment (Spreitzer, 1995) offers insights into the cognitive and motivational factors that shape managerial behavior, particularly perceptions of competence, autonomy, and control that may affect attitudes toward debt and risk-taking.

Despite the extensive literature on capital structure, existing evidence on Colombian SMEs remains fragmented across different theoretical perspectives. Most studies have focused on financial explanations, particularly Trade-Off and Pecking Order theories, while comparatively less attention has been devoted to governance-related and behavioral approaches. Consequently, there is limited understanding of how financial, governance, and psychological factors jointly shape capital structure decisions in Colombian SMEs.

To address this gap, this study conducts a semi-systematic literature review to analyze the theoretical and empirical evidence on capital structure decisions in Colombian SMEs from the perspectives of Trade-Off Theory, Pecking Order Theory, Agency Theory, and Psychological Empowerment. By examining the available literature, the study seeks to provide a broader understanding of the financial, governance, and behavioral factors that shape financing decisions in this context. Accordingly, the following research question guides the study: How do Trade-Off Theory, Pecking Order Theory, Agency Theory, and Psychological Empowerment contribute to explaining capital structure decisions in Colombian SMEs?

The remainder of the article is organized as follows. The next section describes the methodological approach adopted for the semi-systematic literature review, including the search strategy, selection criteria, and analysis procedures. The subsequent sections present and discuss the findings from the reviewed literature through the lenses of Trade-Off Theory, Pecking Order Theory, Agency Theory, and Psychological Empowerment. Finally, the article concludes by highlighting the main theoretical contributions, practical implications, limitations, and directions for future research.

Methodology

Research design

This study adopts a qualitative, descriptive, and interpretive approach aimed at analyzing the theoretical and empirical literature on capital structure decisions in Colombian SMEs within the broader context of international evidence related to Trade-Off Theory, Pecking Order Theory, Agency Theory, and Psychological Empowerment.

Methodologically, the study follows a semi-systematic literature review approach. Semi-systematic reviews are particularly suitable for examining complex and multidisciplinary topics that have been addressed through different theoretical perspectives, as they allow the identification, organization, and synthesis of knowledge from diverse streams of research while maintaining a structured and transparent review process (Snyder, 2019). In the context of capital structure decisions in Colombian SMEs, this approach facilitates the examination of financial, governance, and behavioral explanations derived from distinct theoretical traditions.

To ensure transparency, traceability, and replicability throughout the review process, the study followed the PRISMA 2020 guidelines (Preferred Reporting Items for Systematic Reviews and Meta-Analyses) (Page et al, 2021). The review was conducted following the methodological recommendations proposed by Snyder (2019) and Iannizzi et al. (2023), combining a structured search and selection procedure with an interpretive synthesis of the theoretical and empirical evidence identified in the literature.

Databases and search strategy

The bibliographic search was conducted between March and May 2025 using the Scopus and Web of Science databases. These databases were selected because they are internationally recognized sources of peer-reviewed research and provide broad coverage of high-quality publications in finance, economics, management, and organizational studies.

Considering that a substantial proportion of the scientific literature on capital structure is published in English, the search equations were primarily constructed in this language using Boolean operators and search criteria applied to titles, abstracts, and keywords. Nevertheless, studies published in Spanish were also considered.

The search equations employed were as follows:

- TITLE-ABS-KEY (“capital structure” AND “trade-off theory” AND SMEs)

- TITLE-ABS-KEY (“capital structure” AND “pecking order theory” AND SMEs)

- TITLE-ABS-KEY (“capital structure” AND “pecking order theory” AND Colombia)

- TITLE-ABS-KEY (“capital structure” AND “trade-off theory” AND Colombia)

- TITLE-ABS-KEY (“capital structure” AND “agency theory” AND SMEs)

- TITLE-ABS-KEY (“capital structure” AND “agency theory” AND Colombia)

- TITLE-ABS-KEY (“psychological empowerment” AND financing decisions)

Additionally, complementary manual searches were conducted through cross-references identified in the initially selected articles, particularly in seminal studies and previous reviews relevant to the Latin American context. Because the literature directly linking Psychological Empowerment to capital structure decisions remains limited, a broader search equation was used to identify studies addressing managerial autonomy, decision-making, and financing-related behaviors that could contribute to understanding the behavioral dimensions of capital structure decisions.

Study selection and analysis

To ensure methodological consistency and thematic relevance, inclusion and exclusion criteria were established in accordance with the eligibility procedures recommended by the PRISMA 2020 guidelines (Iannizzi et al., 2023).

The inclusion criteria were: (1) scientific articles published in indexed academic journals; (2) theoretical studies, empirical research, or literature reviews related to capital structure; (3) studies addressing at least one of the four theoretical perspectives examined in this review Trade-Off Theory, Pecking Order Theory, Agency Theory, or Psychological Empowerment; (4) publications written in English or Spanish; and (5) documents published between 2000 and 2025.

The exclusion criteria comprised: (1) book chapters, conference proceedings, dissertations, and other non-peer-reviewed academic documents; (2) studies unrelated to capital structure decisions; (3) publications written in languages other than English or Spanish; and (4) studies published outside the selected time period.

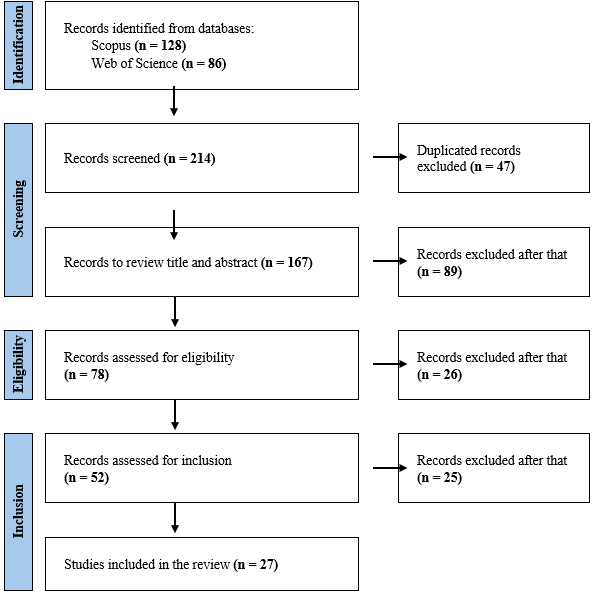

The PRISMA flow diagram summarizes the study selection process. The initial search identified 214 records, including 128 documents from Scopus and 86 from Web of Science. After removing 47 duplicate records, 167 documents remained for title and abstract screening. Subsequently, 89 records were excluded because they did not meet the objectives or eligibility criteria of the review. The remaining 78 studies were assessed through full-text analysis, resulting in the exclusion of 26 additional documents. Consequently, 52 studies advanced to the inclusion stage, and after a final evaluation, 27 documents met all eligibility criteria and were retained for detailed analysis. Figure 1 presents the complete PRISMA flow diagram.

Figure 1

PRISMA flow diagram of the study selection process

Source: Prepared by the authors based on the PRISMA 2020 guidelines.

Figure 1 summarizes the study selection process following the PRISMA 2020 guidelines. The bibliographic search conducted in Scopus and Web of Science identified 214 records, including 128 documents from Scopus and 86 from Web of Science. During the screening stage, 47 duplicate records were removed, resulting in 167 unique documents.

Subsequently, the titles and abstracts of the remaining records were reviewed according to the inclusion and exclusion criteria established for this study. At this stage, 89 records were excluded because they did not address capital structure decisions, were unrelated to the theoretical perspectives examined, or were not aligned with the objectives of the review. As a result, 78 studies advanced to the eligibility stage.

The full texts of these studies were then assessed in detail. During the eligibility assessment, 26 documents were excluded due to limited relevance to capital structure decisions, insufficient theoretical development, or lack of alignment with the scope of the review. The remaining 52 studies were subjected to a final assessment of inclusion, leading to the exclusion of an additional 25 documents because of overlap in findings, limited analytical contribution, or insufficient relevance to the Colombian and emerging economy context. Consequently, 27 studies were retained for detailed analysis.

The final sample constituted the documentary basis of the review. Each study was systematically examined through content analysis and thematic analysis, following the recommendations of Bowen (2009) and Vaismoradi et al. (2013). Initially, the selected studies were organized according to their theoretical perspective, geographical context, methodological approach, and type of contribution. Subsequently, recurrent patterns, theoretical convergences, contextual differences, and research gaps were identified.

The analytical categories were developed through an iterative coding process. First, the studies were classified according to their primary theoretical perspective. Second, similarities and differences across studies were identified and grouped into broader thematic clusters. Finally, the categories were refined to capture both international and Colombian evidence, as well as the governance and behavioral dimensions associated with capital structure decisions.

This process resulted in seven analytical categories: (1) Trade-Off Theory; (2) Pecking Order Theory; (3) Comparative Perspectives on Capital Structure; (4) Agency Theory; and (5) Psychological Empowerment. Additionally, the analysis identified emerging themes related to financial constraints, managerial behavior, information asymmetries, corporate governance, and behavioral factors influencing financing decisions.

This study presents several limitations. First, although the review followed the PRISMA 2020 guidelines to ensure transparency and methodological rigor, it retains an interpretive character and therefore does not incorporate statistical procedures or quantitative synthesis techniques. Second, the review was restricted to Scopus and Web of Science, which may have excluded relevant regional studies not indexed in these databases. Nevertheless, priority was given to the academic quality, visibility, and methodological traceability of the selected sources. Finally, the conceptual and methodological heterogeneity of the reviewed studies limits direct comparison across empirical findings, particularly in research conducted within emerging economies and diverse organizational contexts.

Results

The following section presents the main findings of the semi-systematic literature review. The results are organized according to the four theoretical perspectives examined in this study Trade-Off Theory, Pecking Order Theory, Agency Theory, and Psychological Empowerment as well as comparative contributions that connect different approaches to capital structure. The purpose of this section is to summarize the international and Colombian evidence identified in the selected studies.

Trade-off theory

Research grounded in the Trade-Off Theory (TO) has largely focused on identifying the balance between the benefits and costs of debt that maximizes firm value.

Sabiwalsky (2010) developed a nonlinear model showing that the optimal debt level is reached when the present value of tax shields equals the expected cost of insolvency. The study also highlights the importance of firm size, indicating that larger firms tend to sustain higher leverage ratios.

Similarly, Dierker et al. (2019), using data from more than 82,000 U.S. firms between 1971 and 2011, found that firms are more likely to issue equity when perceived risk increases and to rely on debt when risk decreases.

In Colombia, Chacón et al. (2007), studying 233 SMEs from Bucaramanga, reported debt levels below those predicted as optimal by the theory. Likewise, Zambrano and Acuña (2011), analyzing Coservicios S.A. E.S.P. between 2007 and 2011, found that the Pecking Order framework explained financing decisions more effectively than the Trade-Off model.

Pecking order theory

The Pecking Order Theory (PO) has been widely tested across different countries and industries.

Chen et al. (2013), using panel data from Taiwanese firms, found partial support for PO assumptions, particularly during periods of weak market performance. Agliardi et al. (2016) reported that firms tend to retain earnings rather than seek external financing when investors exhibit greater aversion to uncertainty.

Additional evidence has been reported in both developed and emerging economies. Jiang et al. (2017) observed lower agency costs when ownership was concentrated in a non-managerial majority shareholder. Park and Jang (2018) confirmed the PO framework in U.S. restaurant firms, while Bhama et al. (2018) found stronger adherence to PO predictions among profitable Indian firms. Similar findings were reported in Brazil (Zeidan et al., 2018) and Turkey (Yildirim & Celik, 2021).

In the Colombian context, Arévalo et al. (2022) analyzed 1,548 firms from the agriculture, transportation, tourism, and food sectors between 2017 and 2020. Their findings supported the PO framework in agriculture and tourism but not in transportation and storage.

Comparative perspectives on capital structure

Several studies have compared the explanatory capacity of different capital structure theories.

Berlingeri (2005) compared the Trade-Off and Pecking Order frameworks and proposed the Proactive Trade-Off Model (TOP), which incorporates dynamic financing adjustments. Frank and Goyal (2008) synthesized contributions from Modigliani and Miller, Trade-Off Theory, and Pecking Order Theory, emphasizing the role of adverse selection and agency costs in financing decisions.

Similarly, Carvajal et al. (2018) analyzed firms in Ecuador’s accommodation and food sector and found that smaller firms relied primarily on internal financing, whereas larger firms made greater use of debt financing.

Agency theory

Agency Theory contributes to understanding financing decisions through the analysis of principal-agent relationships and information asymmetries.

Samman and Santos (2009) conceptualized agency as the ability to act autonomously and influence desired outcomes. Partyka (2021) applied the theory to supply chain relationships, identifying governance mechanisms that reduce information asymmetries. Davis et al. (2021) examined agency dynamics in social entrepreneurship, while Van Wijk et al. (2013) analyzed the influence of cultural and network factors. Solomon et al. (2021) linked agency relationships to entrepreneurial motivation and innovation.

In Colombia, Torres et al. (2025) found that SMEs frequently rely on internal financing and trust-based governance arrangements to manage financial activities.

Psychological empowerment and behavioral dimensions

Psychological Empowerment (PE) introduces a behavioral perspective to the study of financing decisions. Based on the work of Thomas and Velthouse (1990) and Spreitzer (1995), this perspective focuses on perceptions of meaning, competence, self-determination, and impact.

Hall (2008) found that empowerment improves managerial performance when organizational systems support autonomy and role clarity. Monje et al. (2021) reported positive effects of empowerment on work engagement, while Ochoa and Coello (2022) highlighted the relationship between empowerment, entrepreneurship, and digital competencies. Similarly, Juyumaya (2022) identified empowerment as an important motivational factor among female social entrepreneurs.

Although empirical evidence directly linking Psychological Empowerment to capital structure decisions remains limited, the reviewed studies highlight the relevance of behavioral and motivational factors in managerial decision-making.

The findings presented above reveal different but complementary perspectives on capital structure decisions. To facilitate comparison across studies and theoretical approaches, Table 1 summarizes the main international and Colombian evidence identified in the literature, highlighting the principal contributions and implications of each perspective for understanding financing decisions in SMEs.

Table 1

Global and Colombian Evidence on Capital Structure

Theory |

International |

Colombian |

Key Insights / Implications |

Trade-Off Theory (TO) |

Sabiwalsky (2010) identifies optimal debt when the net present value of tax shields equals insolvency costs. Dierker, et al (2019) confirm that firms increase equity when risk rises and debt when risk decreases. |

Chacón et al. (2007) find that Colombian SMEs maintain debt levels below optimal. Zambrano & Acuña (2013) observe that TO has limited explanatory power compared to PO. |

The TO holds conceptually but is constrained by limited credit access, small firm size, and risk aversion in Colombian SMEs. |

Pecking Order Theory (PO) |

Chen et al. (2013) and Bhama et al. (2018) show that profitability and market conditions determine financing hierarchy; Yildirim & Celik (2021) confirm validity across investment levels. |

Arévalo et al. (2022) validate PO in agriculture and tourism sectors but not in transport and storage. |

PO better explains financing behavior of SMEs in contexts with information asymmetry and liquidity constraints. |

Comparative Perspectives on Capital Structure |

Berlingeri (2005) proposes the “Proactive Trade-Off” model integrating TO and PO. Frank & Goyal (2008) provide a comprehensive synthesis linking adverse selection and agency costs. Carvajal et al. (2018) find small firms follow PO and large firms TO. |

— |

Firms may combine both TO and PO behaviors, suggesting that financial choices evolve dynamically based on size, profitability, and access to capital markets. |

Agency Theory (AT) |

Jiang et al. (2017) and Partyka (2021) show that ownership concentration reduces agency costs. Davis et al. (2021) and Van Wijk et al. (2013) analyze cultural and relational factors influencing agency dynamics. |

Agency relationships in Colombian SMEs are often informal; Torres, et al. (2025) find that firms rely heavily on internal funds and trust-based governance. |

Agency costs and governance informality strongly influence financing decisions, highlighting the role of ownership structure and trust. |

Psychological Empowerment (PE) |

Spreitzer (1995), Hall (2008), Monje et al. (2021), and Ochoa et al. (2022) link empowerment to motivation, autonomy, and digital competences. |

(Limited empirical evidence in Colombia) |

Incorporating PE provides a behavioral lens to explain how managerial cognition and motivation affect financing behavior, suggesting a key research opportunity. |

Source: Prepared by the authors based on the reviewed literature.

Table 1 provides a comparative synthesis of the evidence identified in the review and illustrates the different contributions of Trade-Off Theory, Pecking Order Theory, Agency Theory, and Psychological Empowerment to the understanding of capital structure decisions in Colombian SMEs.

Discussions

The findings of this review confirm that classical financial theories remain useful for understanding firms’ capital structure decisions, although their explanatory power becomes more limited when applied to emerging economies such as Colombia. In line with the propositions of Modigliani and Miller (1958; 1963), subsequent research has emphasized the importance of balancing debt and equity through the Trade-Off Theory. Studies such as Sabiwalsky (2010) and Dierker et al. (2019) show that firm size, risk, and the balance between tax benefits and insolvency costs influence leverage decisions. However, the Colombian evidence reviewed (Chacón et al., 2007; Zambrano & Acuña, 2013) suggests that SMEs frequently maintain debt levels below those predicted by the theory. These findings indicate that access to credit, financing costs, and institutional constraints may limit firms’ ability to achieve theoretically optimal capital structures.

The evidence also indicates that the Pecking Order Theory provides an important explanation for financing decisions in SMEs. International studies (Chen et al., 2013; Agliardi et al., 2016; Bhama et al, 2018; Zeidan et al., 2018; Yildirim & Celik, 2021) show that firms generally prioritize internal financing and resort to external funds only when necessary. In Colombia, Arévalo et al. (2022) found support for the Pecking Order framework in sectors such as agriculture and tourism, although the evidence was not consistent across all industries. These findings suggest that financing preferences are influenced by information asymmetries, liquidity constraints, and sector-specific conditions.

Rather than functioning as competing explanations, the reviewed evidence suggests that Trade-Off and Pecking Order theories operate as complementary frameworks. Berlingeri (2005) argued that firms may adjust their financing behavior dynamically, while Frank and Goyal (2008) emphasized that capital structure decisions are influenced simultaneously by adverse selection, agency costs, and financing preferences. Likewise, Carvajal et al. (2018) found that firm size influences the relative importance of internal financing and debt. Taken together, these studies suggest that Colombian SMEs combine elements of both theories, balancing financial caution with the need to secure resources for growth.

Agency Theory further enriches the analysis by highlighting the role of governance structures, ownership concentration, and information asymmetries in financing decisions. Studies by Jiang et al. (2017), Partyka (2021), Davis et al. (2021), Van Wijk et al. (2013), and Solomon et al. (2021) demonstrate that agency relationships influence organizational behavior through monitoring mechanisms, incentives, and governance arrangements. In the Colombian context, Torres et al. (2025) found that SMEs frequently rely on internal financing and trust-based governance structures to manage financial activities. While these arrangements may reduce monitoring costs, they may also limit access to external financing by reducing transparency and formal accountability mechanisms.

The incorporation of Psychological Empowerment extends the analysis by introducing a behavioral perspective to capital structure decisions. Drawing on the work of Thomas and Velthouse (1990) and Spreitzer (1995), empowerment emphasizes the importance of competence, self-determination, meaning, and impact in managerial decision-making. Empirical evidence provided by Hall (2008), Monje et al. (2021), Ochoa and Coello (2022), and Juyumaya (2022) suggests that empowered managers exhibit greater confidence, adaptability, and willingness to undertake strategic initiatives. Although direct empirical evidence linking Psychological Empowerment and capital structure remains limited, particularly in Colombia, the reviewed literature suggests that managerial autonomy and behavioral factors may influence attitudes toward debt, risk-taking, and financing choices.

Taken together, the findings support a multidimensional understanding of capital structure decisions in Colombian SMEs. Trade-Off Theory and Pecking Order Theory explain the financial logic underlying financing choices; Agency Theory contributes insights regarding governance structures, ownership relationships, and information asymmetries; and Psychological Empowerment highlights the influence of managerial cognition and behavior. Consequently, capital structure decisions appear to be shaped not only by economic optimization but also by organizational characteristics, governance arrangements, and behavioral factors operating within the institutional context of an emerging economy.

Finally, the review identifies important opportunities for future research. The limited empirical evidence connecting Psychological Empowerment with financing decisions highlights the need for additional studies examining the interaction between financial, governance, and behavioral factors in SMEs. Future research could also explore how managerial characteristics, ownership structures, digital capabilities, and institutional conditions influence capital structure decisions across different sectors and emerging economy contexts.

Conclusions

This study analyzed how Trade-Off Theory, Pecking Order Theory, Agency Theory, and Psychological Empowerment contribute to explaining capital structure decisions in Colombian SMEs. The findings indicate that no single theoretical perspective fully explains financing behavior in this context. Rather, capital structure decisions are best understood as the result of the interaction between financial considerations, governance mechanisms, and managerial behavioral factors. While Trade-Off Theory highlights the balance between the benefits and costs of debt, and Pecking Order Theory explains firms’ preference for internal financing under conditions of information asymmetry, both perspectives are constrained by the institutional and financial realities faced by Colombian SMEs.

The review further demonstrates that governance and behavioral dimensions play a significant role in shaping financing decisions. Agency Theory contributes to understanding the influence of ownership structures, trust-based relationships, and information asymmetries, whereas Psychological Empowerment highlights the role of managerial autonomy, competence, and self-determination in financing behavior. Together, these perspectives provide a more comprehensive explanation of how SMEs adapt their financing strategies to the opportunities and constraints of emerging economies.

The main contribution of this study is the development of a multidimensional perspective that combines financial, governance, and behavioral dimensions to explain capital structure decisions in Colombian SMEs. This perspective extends traditional financial explanations by showing that financing choices are not determined exclusively by economic optimization criteria but also by organizational characteristics, managerial perceptions, and institutional conditions. Consequently, the study contributes to the literature by providing a broader framework for understanding capital structure decisions in emerging economies.

From a practical perspective, the findings suggest that improving access to formal credit, strengthening governance practices, and promoting managerial empowerment may contribute to more sustainable financing decisions among SMEs. These actions may enhance firms’ ability to balance growth opportunities with financial stability while increasing their capacity to respond to changing economic conditions.

This study is subject to several limitations. The review was restricted to publications indexed in Scopus and Web of Science and reflects the conceptual and methodological diversity of the available literature. In addition, empirical evidence linking Psychological Empowerment and capital structure remains limited, particularly in the Colombian context.

Future research should empirically examine the interaction between financial, governance, and behavioral factors in SME financing decisions. Particular attention should be given to the role of managerial characteristics, ownership structures, digital capabilities, and institutional conditions in shaping capital structure decisions in emerging economies. Further studies could also evaluate how public policies and organizational practices influence firms’ access to external financing and their long-term financial sustainability.

Ethical considerations

This study is based exclusively on the review of published scientific literature and does not involve human participants, animals, or personal data. Principles of academic integrity were observed through the proper citation and acknowledgment of all sources consulted.

Conflict of interest

The authors declare no conflict of interest.

Author contributions statement

Zuray Melgarejo Molina: research, conceptualization, writing, initial draft, review, and editing of the text.

Mayda Alejandra Calderón Díaz: research, conceptualization, methodology, writing, initial draft, review, and editing of the text.

Felipe Alejandro Torres Castro: research, conceptualization, methodology, formal analysis.

Source of funding

This research received no external funding and was conducted using the authors’ own resources.

References

(1)Agliardi, E., Agliardi, R. & Spanjers, W. (2016). Corporate financing decisions under ambiguity: Pecking order and liquidity policy implications. Journal of Business Research, 69, 6012-6020. http://dx.doi.org/10.1016/j.jbusres.2016.05.016

(2)Arévalo, G., Zambrano, S. & Vásquez, A. (2022). Teoría del Pecking Order para el análisis de la estructura de capital: aplicación en tres sectores de la economía colombiana. Revista Finanzas y Política Económica, 14(1), 99-129. https://revfinypolecon.ucatolica.edu.co/article/view/4295

(3)Berlingeri, H. (2005). ¿Trade Off o Pecking Order? una investigación sobre las decisiones de financiamiento. Poliantea, 2(3), 119-139. https://dialnet.unirioja.es/ejemplar/372770

(4)Bhama, V., Jain, P. & Yadav, S. (2018). Relationship between the pecking order theory and firm’s age: Empirical evidences from India. IIMB Management Review, 30(1), 104-114. https://doi.org/10.1016/j.iimb.2018.01.003

(5)Bowen, G. A. (2009). Document analysis as a qualitative research method. Qualitative Research Journal, 9(2), 27–40. https://doi.org/10.3316/QRJ0902027

(6)Carvajal, A., Michilena, C. & Acuña, G. (2018). Decisiones de financiamiento en empresas del sector de alojamiento y servicios de comida: Trade Off vs. Pecking Order. Revista Killkana Sociales, 2(4), 21-32. https://doi.org/10.26871/killkanasocial.v2i4.96

(7)Chacón, O. P., Arroyo, Y. E. & Villalba, M. L. (2007). Teoría del trade-off para la definición de la estructura de financiación de las pyme’s de Bucaramanga. Revista UIS Ingenierías, 6(2), 9–18. https://revistas.uis.edu.co/index.php/revistauisingenierias/article/view/402

(8)Chen, D., Chen, C., Chen, J. & Huang, Y. (2013). Panel data analyses of the pecking order theory and the market timing theory of capital structure in Taiwan. International Review of Economics and Finance, 27, 1-13. http://dx.doi.org/10.1016/j.iref.2012.09.011

(9)Davis, P. E., Bendickson, J. S., Muldoon, J. & McDowell, W. C. (2021). Agency theory utility and social entrepreneurship: issues of identity and role conflict. Review of Managerial Science, 15, 2299–2318. https://doi.org/10.1007/s11846-020-00423-y

(10)Dierker, M., Lee, I. & Won, S. (2019). Risk changes and external financing activities: Tests of the dynamic trade-off theory of capital structure. Journal of Empirical Finance, 52, 178-200. https://doi.org/10.1016/j.jempfin.2019.03.004

(11)Frank, M. & Goyal, V. (2008). Trade-off and Pecking Order Theories of Debt. Handbook of Empirical Corporate Finance. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=670543

(12)Hall, M. (2008). The effect of comprehensive performance measurement systems on role clarity, psychological empowerment and managerial performance. Accounting, Organizations and Society, 33(2-3), 141-163. https://doi.org/10.1016/j.aos.2007.02.004

(13)Iannizzi, C., Akl, E. A., Anslinger, E., Weibel, S., Kahale, L. A., Aminat, A. M., Piechotta, V. & Skoetz, N. (2023). Methods and guidance on conducting, reporting, publishing, and appraising living systematic reviews: a scoping review. Systematic Reviews, 12(1), 238. https://doi.org/10.1186/s13643-023-02396-x

(14)Jensen, M. & Meckling, W. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305-360. https://doi.org/10.1016/0304-405X(76)90026-X

(15)Jiang, F., Kim, K., Nofsinger, J. & Zhu, B. (2017). A pecking order of shareholder structure. Journal of Corporate Finance, 44, 1-14. http://dx.doi.org/10.1016/j.jcorpfin.2017.03.002

(16)Juyumaya, J. (2022). How psychological empowerment impacts task performance: the mediation role of work engagement and moderating role of age. Front. Psychol, 13, 889936. https://doi.org/10.3389/fpsyg.2022.889936

(17)Modigliani, F. & Miller, M. H. (1958). The Cost of Capital, Corporation Finance and the Theory of Investment. The American Economic Review, 48(3), 261–297. http://www.jstor.org/stable/1809766

(18)Modigliani, F. & Miller, M. H. (1963). Corporate income taxes and the cost of capital: a correction. The American Economic Review, 53(3), 433–443. http://www.jstor.org/stable/1809167

(19)Monje, A., Xanthopoulou, D., Calvo, N. & Abeal, J.P. (2021). Structural empowerment, psychological empowerment, and work engagement: a cross-country study. European Management Journal, 39(6), 779-789. https://doi.org/10.1016/j.emj.2021.01.005

(20)Myers, S. & Majluf, N. (1984). Corporate financing and investment decisions when firms have information that investors do not have. Journal of Financial Economics, 13(2), 187-221. https://doi.org/10.1016/0304-405X(84)90023-0

(21)Ochoa, P. & Coello, D. (2022). Does psychological empowerment mediate the relationship between digital competencies and job performance? Computers in Human Behavior, 140, 107575. https://doi.org/10.1016/j.chb.2022.107575

(22)OECD & ECLAC. (2012). Capítulo 2. Caracterización y políticas de pymes en América Latina. In Perspectivas económicas de América Latina 2013: políticas de pymes para el cambio estructural (pp. 45-70). OCDE. https://www.cepal.org/es/publicaciones/1463-perspectivas-economicas-america-latina-2013-politicas-pymes-cambio-estructural

(23)Page, M. J., McKenzie, J. E., Bossuyt, P. M., Boutron, I., Hoffmann, T. C., Mulrow, C. D., Shamseer, L., Tetzlaff, J. M., Akl, E. A., Brennan, S. E., Chou, R., Glanville, J., Grimshaw, J. M., Hróbjartsson, A., Lalu, M. M., Li, T., Loder, E. W., Mayo-Wilson, E., McDonald, S., ... Moher, D. (2021). The PRISMA 2020 statement: An updated guideline for reporting systematic reviews. BMJ, 372(71). https://doi.org/10.1136/bmj.n71

(24)Park, K. & Jang, S. (2018). Pecking order puzzle: Restaurant firms’ unique financing behaviors. International Journal of Hospitality Management, 70, 99-109. https://doi.org/10.1016/j.ijhm.2017.10.014

(25)Partyka, R. B. (2021). Supply chain management: an integrative review from the agency theory perspective. Revista de Gestão, 29(2), 175-198. https://doi.org/10.1108/REGE-04-2021-0058

(26)Sabiwalsky, R. (2010). Nonlinear modelling of target leverage with latent determinant variables - new evidence on the trade-off theory. Review of Financial Economics, 19(4), 137-150. https://doi.org/10.1016/j.rfe.2010.06.001

(27)Samman, E. & Santos, M.E. (2009). Agency and empowerment: A review of concepts, indicators and empirical evidence. University of Oxford. https://ophi.org.uk/publication/RP-10a

(28)Shyam, L. & Myers, S. (1994). Testing static tradeoff against pecking order models of capital structure. NBER Working Paper Series. National Bureau of Economic Research. Cambridge. https://econpapers.repec.org/paper/nbrnberwo/4722.htm

(29)Snyder, H. (2019). Literature review as a research methodology: an overview and guidelines. Journal of Business Research, 104, 333–339. https://doi.org/10.1016/j.jbusres.2019.07.039

(30)Solomon, S., Bendickson, J. S., Marvel, M. R., McDowell, W. C. & Mahto, R. (2021). Agency theory and entrepreneurship: a cross-country analysis. Journal of Business Research, 122, 466-476. https://doi.org/10.1016/j.jbusres.2020.09.003

(31)Spreitzer, G. M. (1995). Psychological empowerment in the workplace: Dimensions, measurement, and validation. Academy of Management Journal, 38(5), 1442-1465. https://doi.org/10.2307/256865

(32)Thomas, K. W. & Velthouse, B. A. (1990). Cognitive elements of empowerment: An “interpretive” model of intrinsic task motivation. Academy of Management Review, 15(4), 666–681. https://doi.org/10.5465/amr.1990.4310926

(33)Torres, F. A., Calderón, M. A. & Melgarejo, Z. A. (2025). Costo de capital y rentabilidad de los activos de las micro, pequeñas y medianas empresas comerciales (MIPYMES) en Bogotá. Revista UIS Ingenierías, 24(1), 21–36. https://doi.org/10.18273/revuin.v24n1-2025003

(34)Vaismoradi, M., Turunen, H. & Bondas, T. (2013). Content analysis and thematic analysis: Implications for conducting a qualitative descriptive study. Nursing & Health Sciences, 15(3), 398–405. https://doi.org/10.1111/nhs.12048

(35)Van Wijk, J., Stam, W., Elfring, T., Zietsma, C. & den Hond, F. (2013). Activists and incumbents structuring change: The interplay of agency, culture, and networks in field evolution. Academy of Management Journal, 56(2), 358–386. https://doi.org/10.5465/amj.2008.0355

(36)Vera, M. & Mora, E. (2013). Líneas de investigación en micro, pequeñas y medianas empresas. Revisión documental y desarrollo en Colombia. Tendencias, 12(1), 213–226. https://revistas.udenar.edu.co/index.php/rtend/article/view/544

(37)Yildırım, D. & Çelik, A. (2021). Testing the pecking order theory of capital structure: Evidence from Turkey using panel quantile regression approach. Borsa Istanbul Review, 21(4), 317-331. https://doi.org/10.1016/j.bir.2020.11.002

(38)Zambrano, S. y Acuña, G. (2011). Estructura de capital. Evolución teórica. Criterio Libre, 9(15), 81-102. https://dialnet.unirioja.es/servlet/articulo?codigo=3815888

(39)Zambrano, S. & Acuña, G. (2013). Teoría del Pecking Order versus teoría del Trade off para la empresa Coservicios S.A. E.S.P. Apuntes del CENES, 32(56), 205-236. https://dialnet.unirioja.es/servlet/articulo?codigo=4737594

(40)Zeidan, R., Galil, K. & Shapir, O. (2018). Do ultimate owners follow the pecking order theory? The Quarterly Review of Economics and Finance, 67, 45-50. https://doi.org/10.1016/j.qref.2017.04.008